Abstract

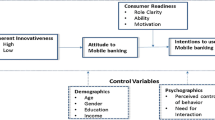

The presumed dominant role of usability attributes (ie usefulness and ease of use) in predicting consumer adoption of a technologically based innovation (eg internet banking — IB) is reexamined, by using an extended framework, which, apart from usability, incorporates the social and psychological aspects of the adoption process. Furthermore, given that IB has been around for almost a decade, it is high time to update the profile of the potential adopters. Results, underscore the role of social factors as predictors of potential IB adopters, whereas the demographic profile of future IB adopters displays important differences compared to that of those already using IB. Possible explanations are discussed, along with implication for practitioners and suggestions for future research.

Similar content being viewed by others

References

Nath, R., Schrick, P. and Parzinger, M. (2001) ‘Banker's perspectives on internet banking’, e-Service Journal, Vol. 1, No. 1, pp. 21–36.

Mols, N. P. (1999) ‘The internet and the banks’ strategic distribution channel decisions’, International Journal of Bank Marketing, Vol. 17, No. 6/7, pp. 295–300.

Akinci, S., Aksoy, S. and Atilgan, E. (2004) ‘Adoption of Internet banking among sophisticated consumer segments in an advanced developing country’, International Journal of Bank Marketing, Vol. 22, No. 3, pp. 212–232.

Shao, G. (2007) ‘The diffusion of online banking: Research trends from 1998 to 2006’, Journal of Internet Banking and Commerce, Vol. 12, No. 2, pp. 1–13.

Rogers, E. M. (1962) ‘Diffusion of Innovations’, The Free Press, New York.

Rogers, E. M. (2003) ‘Diffusion of Innovations’, The Free Press, New York.

Polatoglu, V. and Ekin, S. (2001) ‘An empirical investigation of the Turkish consumers’ acceptance of Internet banking services’, The International Journal of Bank Marketing, Vol. 19, No. 4/5, pp. 156–165.

Howcroft, B., Hamilton, R. and Hewer, P. (2002) ‘Consumer attitude and the usage and adoption of home-based banking in the United Kingdom’, International Journal of Bank Marketing, Vol. 20, No. 3, pp. 111–121.

Kleinbaum, D. G. (1994) ‘Logistic regression: A self-learning text’, Springer-Verlag, New York.

Menard, S. (2002) ‘Applied logistic regression analysis’, 2nd edn, Thousand Oaks, Sage Publications, CA.

Lassar, W. M., Manolis, C. and Lassar, S. S. (2005) ‘The relationship between consumer innovativeness, personal characteristics, and online banking adoption’, International Journal of Bank Marketing, Vol. 23, No. 2, pp. 176–199.

Mäenpää;, K., Kanto, A., Kuusela, H. and Paul, P. (2006) ‘More hedonic versus less hedonic consumption behaviour in advanced internet bank services’, Journal of Financial Services Marketing, Vol. 11, No. 1, pp. 4–16.

Fox, S. and Beier, J. (2006) ‘Online banking 2006: Surfing to the bank’, Pew Internet & American Life Project. (cited 30th June, 2007); Available from: www.pewinternet.org/PPF/r/185/report_display.asp.

Fang, Y. (2006) ‘Forecasting the number of online banking users in China’, China Inforworld, September.

Davis, F. D. (1989) ‘Perceived usefulness, perceived ease of use, and user acceptance of information technology’, MIS Quarterly, Vol. 13, No. 3, pp. 319–339.

King, W. R. and He, J. (2006) ‘A meta-analysis of the technology acceptance model’, Information & Management, Vol. 43, No. 6, pp. 740–755.

Legris, P., Ingham, J. and Collerette, P. (2003) ‘Why do people use information technology? A critical review of the technology acceptance model’, Information & Management, Vol. 40, No. 3, pp. 191–204.

Ma, Q. and Liu, L. (2004) ‘The technology acceptance model: A meta-analysis of empirical findings’, Journal of Organizational and End User Computing, Vol. 16, No. 1, pp. 59–72.

Chan, S. -C. and Lu, M. -T. (2004) ‘Understanding internet banking adoption and use behaviour: A Hong Kong perspective’, Journal of Global Information Management, Vol. 12, No. 3, pp. 21–43.

Chau, P. Y. K. and Lai, V. S. K. (2003) ‘An empirical investigation of the determinants of user acceptance of Internet banking’, Journal of Organizational Computing & Electronic Commerce, Vol. 13, No. 2, pp. 123–145.

Eriksson, K., Kerem, K. and Nilsson, D. (2005) ‘Customer acceptance of internet banking in Estonia’, International Journal of Bank Marketing, Vol. 23, No. 2, pp. 200–216.

Suh, B. and Han, I. (2002) ‘Effect of trust on customer acceptance of Internet banking’, Electronic Commerce Research & Applications, Vol. 1, No. 3/4, pp. 247–263.

McKechnie, S., Winkihofer, H. and Ennew, C. (2006) ‘Applying the technology acceptance model to the online retailing of financial services’, International Journal of Retail & Distribution Management, Vol. 34, No. 4/5, pp. 388–410.

Shugan, S. (2006) ‘Errors in the variables, unobserved Heterogeneity, and other ways of hiding statistical error’, Marketing Science, Vol. 25, No. 3, pp. 203–216.

Moore, G. C. and Benbasat, I. (1991) ‘Development of an instrument to measure the perceptions of adopting an information technology innovation’, Information Systems Research, Vol. 2, No. 3, pp. 192–222.

Agarwal, R. and Prasad, J. (1997) ‘The role of innovation characteristics and perceived voluntariness in the acceptance of information technologies’, Decision Sciences, Vol. 28, pp. 557–582.

Karahanna, E., Straub, D. W. and Chervany, N. L. (1999) ‘Information technology adoption across time: A cross-sectional comparison of pre-adoption and post-adoption beliefs’, MIS Quarterly, Vol. 23, No. 2, pp. 183–213.

Moore, G. C. and Benbasat, I. (1996) ‘Integrating diffusion of innovations and theory of reasoned action models to predict utilization of information technology by end-users’, in Kautz, K. and Pries-Heje, J. (eds) ‘Diffusion and Adoption of Information Technology’, Chapman & Hall, London, pp. 132–146.

Plouffe, C. R., Hulland, J. S. and Vandenbosch, M. (2001) ‘Richness versus parsimony in behaviour technology adoption decisions — Understanding merchant adoption of a smart card-based payment system’, Information Systems Research, Vol. 12, No. 2, pp. 208–222.

Venkatesh, V., Morris, M. G., Davis, G. B. and Davis, F. D. (2003) ‘User acceptance of information technology: Toward a unified view’, MIS Quarterly, Vol. 27, No. 3, pp. 425–478.

Rogers, E. M. (1995) ‘Diffusion of Innovations’, The Free Press, New York.

Konana, P. and Balasubramanian, S. (2005) ‘The Social — Economic — Psychological model of technology adoption and usage: An application to online investing’, Decision Support Systems, Vol. 39, No. 3, pp. 505–524.

Guriting, P. and Ndubisi, N. O. (2006) ‘Borneo online banking: Evaluating customer perceptions and behavioural intention’, Management Research News, Vol. 29, No. 1/2, pp. 6–15.

Lai, V. S. and Li, H. (2005) ‘Technology acceptance model for internet banking: An invariance analysis’, Information & Management, Vol. 42, No. 2, pp. 373–386.

Assael, H. (2005) ‘A demographic and psychographic profile of heavy internet users and users by type of internet usage’, Journal of Advertising Research, Vol. 45, No. 1, pp. 93–123.

Pampel, F. C. (2000) ‘Logistic regression: A primer’, Thousand Oaks, Sage Publications, CA.

Tabachnick, B. G. and Fidell, L. S. (2001) ‘Using Multivariate Statistics’, Harper Collins, New York.

Van Selm, M. and Jankowski, N. W. (2006) ‘Conducting online surveys’, Quality & Quantity, Vol. 40, pp. 435–456.

Annual National Survey of ICT Usage. (2006). Greek Ministry of Development, Press Release. (cited 30th June, 2007); Available from: http://www.ebusinessforum.gr/information/statistics/grnet_statistics/index.php?downid=1519&parent=1272&language=el#1272.

Arbuckle, J. (2006) ‘Amos 7.0 User's Guide’, Amos Development Corporation, Spring House, PA.

Schumacker, R. E. and Lomax, R. G. (2004) ‘A Beginner's Guide to Structural Equation Modeling’, Lawrence Erlbaum Publishers, London.

DeVellis, R. F. (2003) ‘Scale Development: Theory and Applications’, Sage, London.

Calculations based on the first subsample of IB users (n=429), however similar results were obtained when the second subsample of IB users (n=429), and the IB nonusers sample (n=418) were employed.

Fornell, C. and Larcker, D. F. (1981) ‘Structural equation models with unobservable variables and measurement error: Algebra and statistics’, Journal of Marketing Research, Vol. 18, pp. 382–388.

Goldsmith, R. E. and Hofacker, C. F. (1991) ‘Measuring consumer innovativeness’, Journal of the Academy of Marketing Science, Vol. 19, pp. 209–221.

Vijaysarathy, L. R. (2003) ‘Shopping orientations, product types and internet shopping intentions’, Electronic Markets, Vol. 13, No. 1, pp. 67–79.

Field, A. P. (2006) ‘Discovering statistics using SPSS’, Sage Publications, London.

Hair, J. F., Black, B., Babin, B. and Anderson, R. E. (2006) ‘Multivariate Data Analysis’, Prentice-Hall, Englewood Cliffs, NJ.

Hosmer, D. and Lemeshow, S. (1989) ‘Applied Logistic Regression’, Wiley & Sons, New York.

Roselius, R. (1971) ‘Consumer rankings of risk reduction methods’, Journal of Marketing, Vol. 35, No. 1, pp. 56–61.

Burke, R. R. (2002) ‘Technology and the customer interface: What consumers want in the physical and virtual store’, Journal of the Academy of Marketing Science, Vol. 30, No. 4, pp. 411–432.

Murray, K. B. (1991) ‘A test of services marketing theory: Consumer information acquisition activities’, Journal of Marketing, Vol. 55, No. 1, pp. 10–25.

Couper, M. P. (2000) ‘Web surveys: A review of issues and approaches’, Public Opinion Quarterly, Vol. 64, pp. 464–494.

Couper, M. P., Traugott, M. W. and Lamias, M. J. (2001) ‘Web survey design and administration’, Public Opinion Quarterly, Vol. 65, No. 2, pp. 230–253.

Cunningham, L. F., Gerlach, J. and Harper, M. D. (2005) ‘Perceived risk and e-banking services: An analysis from the perspective of the consumer’, Journal of Financial Services Marketing, Vol. 10, No. 2, pp. 165–178.

Heaney, J. -G. (2007) ‘Generations X and Y's internet banking usage in Australia’, Journal of Financial Services Marketing, Vol. 11, No. 3, pp. 196–210.

Littler, D. and Melanthiou, D. (2006) ‘Consumer perceptions of risk and uncertainty and the implications for behaviour towards innovative retail services: The case of Internet Banking’, Journal of Retailing & Consumer Services, Vol. 13, No. 6, pp. 431–443.

Author information

Authors and Affiliations

Appendix

Appendix

Perceived Characteristics of Innovation (Moore and Benbasat39)

Relative Advantage

Using IB speeds up banking (ra1)Using IB improves the quality of banking (ra2) Using IB makes banking easier (ra3) Using IB gives me greater control in banking (ra4) Using IB enhances banking (ra5)

Ease of Use

Overall, I believe that IB is easy to use (eu1) Learning to operate IB is easy for me (eu2) I believe that it is easy to get IB to do what I want it to do (eu3)

Compatibility

Using IB is compatible with all aspects of banking (comp1) Using IB is completely compatible with my current ways of banking (comp2) I think that using IB fits well with the way I like to do banking (comp3)

Image

People who use IB have a high profile (im1) People who use a IB have more prestige than those who do not (im2) Using IB is a status symbol (im3)

Result Demonstrability

I would have no difficulty telling others about the results of using IB (rd1) I would have difficulty explaining why using IB may or may not be beneficial (rd2) The results of using IB are apparent to me (rd3)

Visibility

I have not seen many others using IB (vs1) I have seen what others do using IB (vs2) It is easy for me to observe others using IB (vs3)

Trialability

Before deciding whether to use IB. I can properly try it out (try1) IB is available to me to adequately try it (try2) It is permitted to use IB on a trial basis long enough to see what it can do (try3) I do not really have adequate opportunities to try out different things on IB (try4) Voluntariness My bank does not require me to use IB (vol1) Although it was suggested by my bank. using IB is certainly not compulsory (vol2) My use of IB is voluntary (vol3)

Domain Specific Innovativeness (Goldsmith and Hofacker20)

In general, I am among the last in my circle of friends to visit my bank's new website when it appears on the WWW.

If I heard that my bank's new web was available on the web, I would not be interested enough to visit it. Compared to my friends, I seek out relatively little information over my bank's new website. In general, I am the last in my circle of friends to know of any new bank websites. I will visit a new bank's website even if I have not heard of it before. I know about new bank websites before most other people in my circle do.

Shopping Orientation (Vijayasarathy57)

Economic

I make it a rule to shop at a number of stores before I buy. I can save a lot of money by shopping around. I like to have a great deal of information before I buy. Recreational I like to go shopping with a friend. I often combine shopping with lunch or dinner at a restaurant. Shopping gives me a chance to get out and do something.

Rights and permissions

About this article

Cite this article

Gounaris, S., Koritos, C. Using the extended innovation attributes framework and consumer personal characteristics as predictors of internet banking adoption. J Financ Serv Mark 13, 39–51 (2008). https://doi.org/10.1057/fsm.2008.4

Received:

Revised:

Published:

Issue Date:

DOI: https://doi.org/10.1057/fsm.2008.4