Abstract

Strategic planning in non-life insurance companies must consider differing demands from the company’s various stakeholders. While investors and shareholders require growth in equity market value, rating agencies, costumers and the authorities focus on the company’s solvency, that is, the amount of capital covering the business risks. In that regard, growth in premium income and business profitability are critical, but opposing drivers for operative management. In this article, we model profitability in the insurance business in dependence on premium growth and analyse the impact of the underlying growth strategy on shareholder value and solvency for a non-life insurance company. In a multi-period framework, we find that an optimal growth strategy, maximising net present value and fulfilling a solvency constraint can be derived in dependence on the initial insurance portfolio mix of new and renewal business. The results of the analysis further demonstrate that higher growth rates can lead to lower equity values and vice versa, and that the solvency constraint can prohibit a shareholder-value-maximising strategy. Therefore, the approach is useful in supporting strategic decision-taking and value-based management in non-life insurance companies.

Similar content being viewed by others

Notes

See, for example, the Investors’ Day presentations of the big European insurers Allianz (www.allianz.com), Assicurazioni Generali (www.generali.com) or AXA (www.axa.com).

A comprehensive overview on quantile-based risk measures is provided by Dowd and Blake (2006).

Wang et al. (2011) show the importance of cycle management for an insurer’s growth strategy.

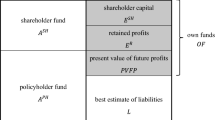

For full compatibility with the NPV in (3) at different periods t, the value of already realized residual income (TVRI) must be added to PVRI t (O’Hanlon and Peasnell, 2002):

.

.Reinsurance is excluded for simplification reasons.

We use an amended version of the approach introduced by Fu (2012).

More complex functions describing non-linear relationships could easily be incorporated instead.

Using the formula for the equilibrium state of new business percentage provided by Fu (2012), we obtain

.

.For simplification reasons, we assume LR0/CR0=LR t /CR t =const and ER0/CR0=ER t /CR t , when developing the financial statements. Alternatively, fixed percentages for the business expenditure or cost functions, in dependence on growth, could be applied.

Data obtained from www.allianz.com/investor_relations at 1 April 2015.

In the technical specifications for non-life underwriting risk modelling, EIOPA (2013, section SCR.9.2.) defines constant standard deviations for premium and reserve risk for different lines of business. In our model framework, v represents all risks of the insurer and is therefore assumed to have a value exceeding those specified by EIOPA (2013, section SCR.9.2.) for the single lines of business.

The premium growth rates in the German non-life insurance market range from -0.9 per cent to 3.5 per cent in the years 2003-2013 (German Insurance Association, 2014).

In the model framework, the impact of the initial parameter values on the results, and therefore, possible levers for strategic measures for management could be observed by a sensitivity analysis. Accordingly, we provide a sensitivity analysis of the model outcomes by varying the initial parameter values in Table 1 with +1 per cent. The related impact on (optimal) growth, net present value (at its maximum) and solvency level is depicted in relation to the results of the base scenario as a percentage. Figure A1 visually illustrates the results of the sensitivity analysis.

.

. .

.References

Biger, N. and Kahane, Y. (1978) ‘Risk considerations in insurance ratemaking’, The Journal of Risk and Insurance 45 (1): 121–132.

Butsic, R.P. (1994) ‘Solvency measurement for property-liability risk-based capital applications’, The Journal of Risk and Insurance 61 (4): 656–690.

Cohen, A. (2005) ‘Asymmetric information and learning: Evidence from the automobile insurance market’, The Review of Economics and Statistics 87 (2): 197–207.

Cummins, J.D. and Harrington, S. (1985) ‘Property-liability insurance rate regulation: Estimation of underwriting betas using quarterly profit data’, The Journal of Risk and Insurance 52 (1): 16–43.

Cummins, J.D. and Sommer, D.W. (1996) ‘Capital and risk in property-liability insurance markets’, Journal of Banking & Finance 20 (6): 1069–1092.

D’Arcy, S.P. and Doherty, N.A. (1989) ‘The aging phenomenon and insurance price’, Proceedings of the Casualty Actuarial Society, 76(145), pp. 24–44.

D’Arcy, S.P. and Doherty, N.A. (1990) ‘Adverse selection, private information and lowballing in insurance markets’, The Journal of Business 63 (2): 145–164.

D’Arcy, S.P. and Gorvett, R.W. (2004) ‘The use of dynamic financial analysis to determine whether an optimal growth rate exists for a property-liability insurer’, The Journal of Risk and Insurance 71 (4): 583–615.

Diers, D. (2011) ‘Management strategies in multi-year enterprise risk management’, The Geneva Papers on Risk and Insurance—Issues and Practice 36 (1): 107–125.

Diers, D., Eling, M., Kraus, C. and Reuss, A. (2012) ‘Market-consistent embedded value in non-life insurance: How to measure it and why’, The Journal of Risk Finance 13 (4): 320–346.

Dowd, K. and Blake, D. (2006) ‘After VaR: The theory, estimation, and insurance applications of quantile-based risk measures’, The Journal of Risk and Insurance 73 (2): 193–229.

EIOPA (2013) Technical Specification on the Long Term Guarantee Assessment (Part I), EIOPA-DOC-13/061, Frankfurt: European Insurance and Occupational Pensions Authority.

EIOPA (2014) The Underlying Assumptions in the Standard Formula for the Solvency Capital Requirement Calculation, EIOPA-14-322, Frankfurt: European Insurance and Occupational Pensions Authority.

Eling, M. and Parnitzke, T. (2007) ‘Dynamic financial analysis: Classification, conception, and implementation’, Risk Management and Insurance Review 10 (1): 33–50.

Eling, M., Schmeiser, H. and Schmit, J.T. (2007) ‘The Solvency II process: Overview and critical analysis’, Risk Management and Insurance Review 10 (1): 69–85.

European Commission (2009) ‘Solvency II Framework Directive: Directive 2009/138/EC’, 25 November.

Fairley, W.D. (1979) ‘Investment income and profit margins in property-liability insurance: Theory and empirical results’, The Bell Journal of Economics 10 (1): 192–210.

Feldblum, S. (1996) ‘Personal automobile premiums: an asset share pricing approach for property/casualty insurance’, Proceedings of the Casualty Actuarial Society, 83(158 & 159), pp. 190–296.

Fu, L. (2012) ‘Optimal growth for P&C insurance companies’, Variance 6 (1): 102–121.

German Insurance Association (GDV) (2014) Statistical Yearbook of German Insurance 2014, Karlsruhe: German Insurance Association (GDV).

Hill, R.D. (1979) ‘Profit regulation in property-liability insurance’, The Bell Journal of Economics 10 (1): 172–191.

Inselbag, I. and Kaufold, H. (1997) ‘Two DCF approaches for valuing companies under alternative financing strategies (and how to choose between them)’, Journal of Applied Corporate Finance 10 (1): 114–122.

Kraus, C. (2013) ‘EVA / RAROC vs. MCEV earnings: A unification approach’, The Geneva Papers on Risk and Insurance—Issues and Practice 38 (1): 1 113–136.

Lintner, J. (1965) ‘The valuation of risk assets and the selection of risky investments in stock portfolios and capital budgets’, The Review of Economics and Statistics 47 (1): 13–37.

Ma, Y.-L. and Ren, Y. (2012) ‘Do publicly traded property-casualty insurers cater to the market?’ The Journal of Risk and Insurance 79 (2): 415–430.

Malmi, T. and Ikäheimo, S. (2003) ‘Value based management practices—some evidence from the field’, Management Accounting Research 14 (3): 235–254.

Mossin, J. (1966) ‘Equilibrium in a capital asset market’, Econometrica 34 (4): 768–783.

Nakada, P., Shah, H., Koyluoglu, H.U. and Collignon, O. (1999) ‘P&C RAROC: A catalyst for improved capital management in the property and casualty insurance industry’, The Journal of Risk Finance 1 (1): 52–69.

O’Hanlon, J. and Peasnell, K. (1998) ‘Wall Street’s contribution to management accounting: The Stern Stewart EVA® financial management system’, Management Accounting Research 9 (4): 421–444.

O’Hanlon, J. and Peasnell, K. (2002) ‘Residual income and value-creation: The missing link’, Review of Accounting Studies 7 (2–3): 229–245.

Oletzky, T. and Graf von der Schulenburg, M. (1998) ‘Shareholder value management strategie in Versicherungsunternehmen’, Zeitschrift für die gesamte Versicherungswissenschaft 87 (1/2): 65–93.

Schmautz, M. and Lampenius, N. (2013) ‘Deriving the minimal amount of risk capital for property-liability insurance companies utilizing asset liability management’, Journal of Risk 15 (4): 35–55.

Sharpe, W.F. (1964) ‘Capital asset prices: A theory of market equilibrium under conditions of risk’, The Journal of Finance 19 (3): 425–442.

Stewart III, G.B. (1994) ‘EVA: Facts and fantasy’, Journal of Applied Corporate Finance 7 (2): 71–84.

Tasche, D. (2002) ‘Expected shortfall and beyond’, Journal of Banking & Finance 26 (7): 1519–1533.

Wakker, P., Thaler, R. and Tversky, A. (1997) ‘Probabilistic insurance’, Journal of Risk and Uncertainty 15 (1): 7–28.

Wang, S.S., John, A.M., Hucheng, P. and Weng, K.L. (2011) ‘U.S. property-casualty: Underwriting cycle modeling and risk benchmarks’, Variance 5 (2): 91–114.

Wu, C.-S.P. and Lin, H. (2009) ‘Large scale analysis of persistency and renewal discounts for property and casualty insurance’, CAS E-Forum, Winter 2009, pp. 396–408.

Author information

Authors and Affiliations

Appendix

Appendix

See Figure A1.

Sensitivity analysis.

SeeTable A1, A2, A3, A4 and A5

Rights and permissions

About this article

Cite this article

Schmautz, M. Value Creation and Solvency: A Simple Approach to Deriving a Non-Life Insurer’s Optimal Growth Strategy. Geneva Pap Risk Insur Issues Pract 40, 701–719 (2015). https://doi.org/10.1057/gpp.2015.20

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1057/gpp.2015.20