Abstract

This paper examines the relationship between fiscal policy and the current account, drawing on a large sample of advanced, emerging, and low-income economies and using a variety of statistical methods: panel regressions, an analysis of large fiscal policy and current account changes, and panel vector autoregressions (VAR). On average, across estimation methods, a strengthening in the fiscal balance by 1 percentage point of GDP is associated with a current account improvement of about 0.3 percentage point of GDP. With our preferred estimation method (quarterly structural VAR using government consumption to identify fiscal policy shocks), the relationship is stronger, in the 0.3–0.5 range. The association is stronger in emerging markets and low-income countries; in economies that are more open to trade; and when the economy is somewhat overheated to begin with. The effect is, however, notably weaker during episodes of large fiscal policy and current account changes, suggesting that fiscal policy may have a more limited role in correcting large external imbalances.

Similar content being viewed by others

Notes

The paper primarily analyzes association between changes in overall fiscal policy and the current account for an individual country. It does not delve into questions about the global transmission of fiscal policy shocks.

The marginal rate of substitution between the home and foreign country private consumption must be mirrored by the real exchange rate. Thus, a rise in current home private consumption (relative to the rest of the world) implies a real depreciation of the home currency.

In previous versions of the paper as well as in Supplementary Appendix I (available via the journal website), we provide a tabular summary of the empirical literature.

In this section we restrict the analysis to non-oil-exporting economies partly because of the strong association between the fiscal balance and the current account due to oil price changes simultaneously impacting tax revenues and exports but also because of data availability: the use of cyclically adjusted primary balance reduces the sample of countries.

In developing economies, the direction of the bias is less easy to predict. Indeed in export-led economies, growth shocks would imply a co-movement in fiscal and external balances, whereas external financing constraints accompanying say, an adverse growth shock, could induce corrections in both fiscal and current account deficits.

The following were included in all regressions: a constant term; the lag of the current-account-to-GDP ratio (to control for year-to-year persistence in the current account); the lag of per capita PPP GDP (to control for current account movements related to income convergence); year dummies (to control for common shocks across countries); and fixed country effects (as Hausman test did not support random effects). In regressions 3–7, noninteracted dummies were included to allow for heterogeneous intercepts. The results are almost identical with GMM (system) methods that address the estimation bias arising from the inclusion of the lagged dependent variable. Robustness to outliers was ensured by dropping all observations where either the absolute value of the current account ratio or the CAPB ratio was above 20 percentage points.

An alternative interpretation could be in times of economic crisis, private consumption collapses much more than government consumption, which translates into a stronger current account, while the fiscal balances deteriorate.

We explored but did not find any turning point with public-debt-to-GDP ratios, either for developing economies or for advanced economies. This is not surprising given the weak reporting on public debt ratios in most developing economies for much of the sample period. For advanced economies, it is plausible that a turning point does exist, but was not breached substantially during 1970–2007. Recall that this was a period during which although public debts rose, they were generally low by historical standards, so that debt sustainability alarms were not materially sounded.

The extraction and listing of the episodes is detailed in Supplementary Appendix II provided on the journal website.

Studying the individual episodes, we can, in fact, confirm that the real exchange rate response to fiscal policy changes is nil in advanced economies but supportive in emerging economies.

The list of countries included in our sample can be found in Supplementary Appendix III available on the journal website.

In the results presented in the paper we include the output gap when using quarterly data and the log of the real GDP when using annual data. We have also run a specification for quarterly data using real GDP. But with shorter time series our estimates were affected by the nonstationarity of the output series. Although the results were qualitatively similar over the first quarters, the responses were in many cases explosive after 5 or 10 quarters.

The standard mean-differencing method to remove fixed effects would bias coefficient because of the correlation between lagged dependent variable regressors and fixed effects, The Helmert transformation avoids this problem by using forward mean-differencing.

The coefficients matrix A0 reflects contemporaneous relationships among the variables in Z t . It is not possible to estimate A0 and therefore identify the innovations ɛ t without further assumptions. Therefore, we assume that A0 is a lower triangular matrix.

For the estimation of our panel VAR we use the Stata programs of Love and Ziccino (2006) available on their website. The estimation method is GMM and the error bands are generated using Monte Carlo simulations.

We are referring here to discretionary changes in taxes. Of course, taxes are likely to react to changes in output via automatic stabilizers, but given that response of output is small this will not represent a large change in the budget balance.

The cutoff is calculated for the average over the whole sample.

How restrictive is the assumption that government consumption does not react to output within a year? Corsetti, Meier, and Müller (2010) discuss this issue in detail and, while it might be that during the 2008–09 crisis governments reacted quickly to economic conditions (maybe as fast as 5 to 8 months), this is more of the exception than the norm. Indeed, budgets are done on an annual basis and changes during the fiscal year are more cumbersome. In fact, the evidence from VARs that use quarterly data show that in response to output shocks the response of government consumption is small and insignificant over the first quarters (in most cases it remains insignificant at any horizon). In addition, Corsetti, Meier, and Müller (2010) also justify the use of annual data on the grounds that spending shocks might be foreseeable.

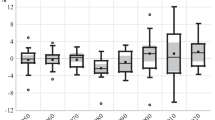

If we exclude the oil exporters (not shown in the figure), in response to a 1 percentage point of GDP increase in government consumption, the current account worsens by 0.20 percentage points of GDP during the year of the shock and 0.24 percentage points of GDP one year after the shock. The impact gradually peters out and becomes insignificant after four years for the sample that excludes the oil exporters. The somewhat stronger response in a sample consisting of emerging and low-income economies only, compared with the full sample, is consistent with the view that the import content of government consumption is higher, and the relative price channel more important, in emerging and developing economies than is the case for advanced economies.

Although not reported in the paper we have also performed the split between more and less open economies using annual data. The results are in line with those using quarterly data.

References

Abbas, S.M. Ali, Nazim Belhocine, Asmaa El-Ganainy, and Mark Horton, 2010, “A Historical Public Debt Database,” IMF Working Paper 10/245 (Washington, DC: International Monetary Fund).

Abiad, Abdul, Daniel Leigh, and Ashoka Mody, 2009, “Financial Integration, Capital Mobility, and Income Convergence,” Economic Policy, Vol. 24, No. 58, pp. 241–305.

Blanchard, Olivier, and R. Perotti, 2002, “An Empirical Characterization of the Dynamic Effects of Changes in Government Spending and Taxes on Output,” Quarterly Journal of Economics, Vol. 117, No. 4, pp. 1329–1368.

Baxter, Marianne, 1995, “International Trade and Business Cycles,” in Handbook of International Economics, Vol. 3, ed. by G.M. Grossmann and K. Rogoff (Amsterdam: North-Holland), pp. 1801–1864.

Bluedorn, John C., and Daniel Leigh, 2011, “Revisiting the Twin Deficits hypothesis: The Effect of Fiscal Consolidation on the Current Account,” manuscript.

Beetsma, Roel, Massimo Giuliodori, and Franc Klaassen, 2007, “The Effects of Public Spending Shocks on Trade Balances and Budget Deficits in the European Union,” Journal of the European Economic Association, Vol. 6, Nos. 2–3, pp. 414–423.

Corsetti, Giancarlo, André Meier, and Gernot J. Müller, 2010, “What Determines Government Spending Multipliers?” Unpublished manuscript.

Corsetti, Giancarlo, and Gernot J. Müller, 2006, “Budget Deficits and Current Accounts: Openness and Fiscal Persistence,” Economic Policy, Vol. 21, No. 48, pp. 597–638.

Devries, Pete, Jaime Guajardo, Daniel Leigh, and Andrea Pescatori, 2011, “A New Action-based Dataset of Fiscal Consolidation,” IMF Working Paper.

Fatas, Antonio, and Ilian Mihov, 2001, “Fiscal Policy and Business Cycles: An Empirical Investigation,” Moneda y Credito, 212.

Feyrer, James, and Jay Shambaugh, 2009, “Global Savings and Global Investment: The Transmission of Identified Fiscal Shocks,” Dartmouth College and NBER (Cambridge, Massachusetts: National Bureau of Economic Research).

Fleming, Marcus J., 1962, “Domestic Financial Policies Under Fixed and Under Floating Exchange Rates,” International Monetary Fund Staff Papers, Vol. 9, pp. 369–379.

Frenkel, Jacob A., and Assaf Razin, 1996, Fiscal Policies and Growth in the World Economy (Cambridge, Massachusetts: MIT Press).

Giavazzi, F., and M. Pagano, 1990, “Can Severe Fiscal Contractions be Expansionary? Tales of Two Small European Countries,” in NBER Macroeconomics Annual 1990, ed. by O. Blanchard and S. Fischer (Cambridge, Massachusetts: MIT Press).

Giavazzi, F., and M. Pagano, 1996, “Non-Keynesian Effects of Fiscal Policy Changes: International Evidence and the Swedish Experience,” Swedish Economic Policy Review, Vol. 3, No. 1, pp. 67–103.

Ilzetzki, Ethan, Enrique Mendoza, and Carlos A. Vegh, 2009, “How Big (Small?) are Fiscal Multipliers?” Unpublished manuscript.

International Monetary Fund, 2008, Exchange Rate Assessments: CGER Methodologies, IMF Occasional Paper No. 261 (Washington: International Monetary Fund).

Khalid, Ahmen M., and Teo W. Guan, 1999, “Causality Tests of Budget and Current Account Deficits: Cross-Country Comparisons,” Empirical Economics, Vol. 24, pp. 389–402.

Lane, Philip R., and Gian M. Milesi-Ferretti, 2006, “The External Wealth of Nations Mark II: Revised and Extended Estimates of Foreign Assets and Liabilities, 1970–2004,” IMF Working Paper No. 06/69 (Washington: International Monetary Fund).

Lane, Philip R., 2010, “External Imbalances and Fiscal Policy,” IIIS Discussion Paper No. 314 (Institute for International Integration Studies, Trinity College Dublin and CEPR).

Love, Inessa, and Lea, Ziccino, 2006, “Financial Development and Dynamic Investment Behavior: Evidence from Panel VAR,” The Quarterly Review of Economics and Finance, Vol. 46, pp. 190–210.

Mohammadi, Hassan, 2004, “Budget Deficits and the Current Account Balance: New Evidence from Panel Data,” Journal of Economics and Finance, Vol. 28, No. 1 (Spring), pp. 39–45.

Monacelli, Tomasso, and Roberto, Perotti, 2006, “Fiscal Policy, the Trade Balance and the Real Exchange Rate: Implications for International Risk Sharing,” Manuscript, IGIER - Bocconi.

Monacelli, Tommaso, and Roberto Perotti, 2007, “Fiscal Policy, the Trade Balance, and the Real Exchange Rate: Implications for International Risk Sharing,” Università Bocconi, Milan, Italy.

Mundell, Robert A., 1963, “Capital Mobility and Stabilizing Policy Under Fixed and Flexible Exchange Rates,” Canadian Journal of Economics and Political Science, Vol. 29, pp. 475–485.

Obstfeld, Maurice, and Kenneth Rogoff, 1996, Foundations of International Macroeconomics (Cambridge, Massachusetts: MIT Press).

Ravn, Morten O., Stephanie Schmitt-Grohe, and Martin Uribe, 2007, Explaining the Effects of Government Spending Shocks on Consumption and the Real Exchange Rate (Durham, North Carolina: Duke University).

Romer, Christina, and David Romer, 2011, “The Macroeconomic Effects of Tax Changes: Estimates Based on a New Measure of Fiscal Shocks,” American Economic Review, Vol. 100, June, pp. 763–801.

Salter, Wilfred A., 1959, “Internal and External Balance: The Role of Price and Expenditure Effects,” Economic Record, Vol. 35, pp. 226–238.

Sancak, Cemile, Ricardo Velloso, and Jing Xing, 2010, “Tax Revenue Response to the Business Cycle,” IMF Working Paper No. 10/71 (Washington, DC).

Additional information

Supplementary Information accompanies the paper on IMF Economic Review website (http://www.palgrave.com/imfer)

A current version of the dataset is available publically in electronic format on the Fiscal Monitor Webpage of IMF.ORG, http://www.imf.org/external/pubs/ft/wp/2010/data/wp10245.zip.

*Abbas, Mauro, and Velloso are in the IMF's Fiscal Affairs Department. Bouhga-Hagbe is in the IMF's Western Hemisphere Department. Fatás is Professor of Economics at INSEAD. The authors are grateful to Carlo Cottarelli for suggesting the topic and constructive comments, the IMF Economic Review editor and two anonymous referees, Philip Gerson and participants in the workshop on External Imbalances and Public Finances at the European Commission, November 2009 for helpful comments; and Sukhmani Bedi and Junhyung Park for excellent research support.