Abstract

European global banks intermediating U.S. dollar funds are important in influencing credit conditions in the United States. U.S. dollar-denominated assets of banks outside the United States are comparable in size to the total assets of the U.S. commercial bank sector, but the large gross cross-border positions are masked by the netting out of the gross assets and liabilities. As a consequence, current account imbalances do not reflect the influence of gross capital flows on U.S. financial conditions. This paper pieces together evidence from a global flow of funds analysis, and develops a theoretical model linking global banks and U.S. loan risk premiums. The culprit for the easy credit conditions in the United States up to 2007 may have been the “Global Banking Glut” rather than the “Global Savings Glut.”

Similar content being viewed by others

Notes

The impact of global liquidity on emerging and developing economies has been explored in Bruno and Shin (2011).

See, for instance, the BIS studies by Baba, McCauley, and Ramaswamy (2009) and McGuire and von Peter (2009) on the use of U.S. dollar wholesale funding by European global banks. Acharya and Schnabl (2009) report that European banks were sponsors for around 70 percent of the asset-backed commercial paper (ABCP) originated prior to the subprime crisis.

See also Obstfeld and Rogoff (2007); Lane and Milesi-Ferretti (2007) and Gourinchas and Rey (2007) and the postcrisis updated evidence in Gourinchas, Govillot, and Rey (2010).

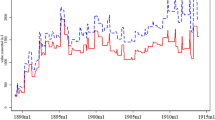

The line numbers in Figure 2 refer to the balance of payments table from the U.S. Bureau of Economic Analysis: www.bea.gov/newsreleases/international/trade/trad_time_series.xls

See for instance Kindleberger's (1965) Princeton Essay in International Finance (Kindleberger, 1965).

Adrian and Shin (2008 and 2010) discuss the evidence from U.S. investment banks, while Bruno and Shin (2011) show in their empirical investigation of capital flows to emerging economies that non-U.S. global banks behave similarly.

See Danielsson et al. (2001) for an early comment on the potential adverse impact of Basel II for financial stability. See also Shin (2010, chapter 10) for historical background.

See BIS (2009) for details on the BIS banking statistics. See McGuire and von Peter (2009) for an example of how the BIS statistics can be used in combination to reconstruct aggregate cross-border banking positions.

The U.S. dollar only series peaks at $4.8 trillion in 2008:Q1, of which $1 trillion is the claim held by branches of U.S. banks on their parent. I am grateful to Carol Bertaut and Laurie DeMarco for pointing this out. See also Cetorelli and Goldberg (2009 and 2011) who document the workings of internal capital markets U.S. banks.

Closely related to the Global Savings Glut argument is the hypothesis that emerging economies lack high-quality financial assets, and that the demand for high quality of assets by emerging economy residents results in current account imbalances and lower interest rates in the United States. See, for instance, Caballero, Fahri, and Gourinchas (2008).

See Adrian and Shin (2008) for a possible microfoundation for the VaR constraint as a consequence of constraints imposed by creditors.

See Adrian and Shin (2008 and 2010) for empirical evidence that banks take equity as given and adjust leverage by adjusting the size of their balance sheet.

This is an assumption made for simplicity of the solution, and does not affect the overall conclusions. If MMF shares are not guaranteed, then the small credit risk in MMF shares will need to be factored into the portfolio decision.

See Vasicek (2002) for additional properties of the asset realization function w(Y).

References

Acharya, Viral, and Philipp Schnabl, 2009, “Do Global Banks Spread Global Imbalances? The Case of Asset-Backed Commercial Paper during the Financial Crisis of 2007-09,” IMF Economic Review, Vol. 58, No. 1, pp. 37–73.

Adrian, Tobias, and Hyun Song Shin, 2008, Procyclical Leverage and Value-at-Risk, Federal Reserve Bank of New York Staff Report 338. Available via the Internet: www.newyorkfed.org/research/staff_reports/sr338.html.

Adrian, Tobias, and Hyun Song Shin, 2010, “Liquidity and Leverage,” Journal of Financial Intermediation, Vol. 19, No. 3, pp. 418–437.

Adrian, Tobias, Paolo Colla, and Hyun Song Shin, 2011, “Which Financial Frictions? Parsing the Evidence from the Financial Crisis of 2007–9,” Working Paper.

Baba, Naohiko, Robert N. McCauley, and Srichander Ramaswamy, 2009, “US Dollar Money Market Funds and Non-US Banks,” BIS Quarterly Review, March, pp. 65–81.

Bank for International Settlements, 2009, Guide to the International Financial Statistics, Available via the Internet: www.bis.org/statistics/intfinstatsguide.pdf.

Bank for International Settlements, 2010, “Funding Patterns and Liquidity Management of Internationally Active Banks,” CGFS Papers 39, Committee on the Global Financial System, May.

Basel Committee on Banking Supervision, 2005, International Convergence of Capital Measurement and Capital Standards: A Revised Framework, Bank for International Settlements, November 2005. Available via the Internet: www.bis.org/publ/bcbs118.pdf.

Bernanke, Ben S., 2005, The Global Saving Glut and the U.S. Current Account Deficit, Remarks at the Sandridge Lecture, Virginia Association of Economists, Richmond, Virginia, March 10, 2005. Available via the Internet: www.federalreserve.gov/boarddocs/speeches/2005/200503102/.

Bernanke, Ben S., Carol Bertaut, Laurie Pounder DeMarco, and Steven Kamin, 2011, International Capital Flows and the Returns to Safe Assets in the United States, 2003–2007, International Finance Discussion Papers Number 1014, Board of Governors of the Federal Reserve System. Available via the Internet: www.federalreserve.gov/pubs/ifdp/2011/1014/ifdp1014.htm.

Bertaut, Carol, Laurie Pounder DeMarco, Steven Kamin, and Ralph Tryon, 2011, ABS Inflows to the United States and the Global Financial Crisis, Board of Governors of the Federal Reserve System International Finance Discussion Paper 1028, August 2011. Available via the Internet: www.federalreserve.gov/pubs/ifdp/2011/1028/ifdp1028.pdf.

Borio, Claudio, and Piti Disyatat, 2011, “Global Imbalances and the Financial Crisis: Link or No Link?” BIS Working Papers No 346. Available via the Internet: www.bis.org/publ/work346.pdf.

Bruno, Valentina, and Hyun Song Shin, 2011, “Capital Flows, Cross-Border Banking and Global Liquidity,” Working Paper.

Caballero, Ricardo J., Emmanuel Farhi, and Pierre-Olivier Gourinchas, 2008, “An Equilibrium Model of “Global Imbalances” and Low Interest Rates,” American Economic Review, Vol. 98, No. 1, pp. 358–393.

Cetorelli, Nicola, and Linda S. Goldberg, 2009, “Banking Globalization and Monetary Transmission,” Forthcoming in Journal of Finance.

Cetorelli, Nicola, and Linda S. Goldberg, 2011, “Global Banks and International Shock Transmission: Evidence from the Crisis,” International Monetary Fund Economic Review, Vol. 59, No. 1, pp. 41–46.

Danielsson, Jon, others 2001, An Academic Response to Basel II, Financial Markets Group Special Paper 130, London School of Economics. Available via the Internet: www.hyunsongshin.org/www/basel2.pdf.

European Central Bank, 2011, Financial Stability Review, June 2011, ECB Frankfurt. Available via the Internet: www.ecb.eu/pub/fsr/html/index.en.html.

Fleming, J.Marcus, 1962, “Domestic Financial Policies Under Fixed and Floating Exchange Rates,” IMF Staff Papers, Vol. 9, pp. 369–379.

Gilchrist, Simon, and Egon Zakrajsek, 2011, “Credit Spreads and Business Cycle Fluctuations,” Forthcoming in American Economic Review.

Gourinchas, Pierre-Olivier, and Helene Rey, 2007, “International Financial Adjustment,” Journal of Political Economy, Vol. 115, No. 4, pp. 665–703.

Gourinchas, Pierre-Olivier, Nicolas Govillot, and Helene Rey, 2010, “Exorbitant Privilege and Exorbitant Duty,” Working Paper.

Hahm, Joon-Ho, Hyun Song Shin, and Kwanho Shin, 2011, “Non-Core Bank Liabilities and Financial Vulnerability,” Working Paper.

Kindleberger, Charles, 1965, “Balance of Payments Deficits and the International Market for Liquidity,” Princeton Essays in International Finance, No. 46, May 1965. Available via the Internet: www.princeton.edu/126ies/old_series-win.htm.

Lane, Philip, and Gian Maria Milesi-Ferretti, 2007, “The External Wealth of Nations Mark II: Revised and Extended Estimates of Foreign Assets and Liabilities, 1970–2004,” Journal of International Economics, Vol. 73, pp. 223–250.

McGuire, Patrick, and Goetz von Peter, 2009, “The US Dollar Shortage in Global Banking and the International Policy Response,” BIS Working Paper 291 (Bank for International Settlements).

Milesi-Ferretti, Gian Maria, 2009, Notes on the Financial Crisis and Global Financial Architecture, in Causes of the Crisis: Key Lessons, Proceedings of the G20 Workshop on the Global Economy. Mumbai, May 2009. Available via the Internet: www.g20.org/Documents/g20_workshop_causes_of_the_crisis.pdf.

Mundell, Robert A., 1963, “Capital Mobility and Stabilization Policy Under Fixed and Flexible Exchange Rates,” Canadian Journal of Economic and Political Science, Vol. 29, No. 4, pp. 475–485.

Obstfeld, Maurice, 2012a, “Financial Flows, Financial Crises, and Global Imbalances,” Journal of International Money and Finance, Vol. 31, No. 2012, pp. 469–480.

Obstfeld, Maurice, 2012b, Does the Current Account Still Matter? Ely Lecture, delivered at the 2012 American Economic Association meeting. Forthcoming in the American Economic Review Papers and Proceedings, 2012. Available via the Internet: www.elsa.berkeley.edu/126obstfeld/Ely%20lecture.pdf.

Obstfeld, Maurice, and Kenneth Rogoff, 2007, “The Unsustainable U.S. Current Account Position Revisited,” in G7 Current Account Imbalances: Sustainability and Adjustment, ed. by Richard H. Clarida (Chicago: University of Chicago Press (for NBER).

Pozsar, Zoltan, 2011, “Institutional Cash Pools and the Triffin Dilemma of the U.S. Banking System,” IMF Working Paper, WP/11/190, August.

Shin, Hyun Song, 2010, Risk and Liquidity, 2008 Clarendon Lectures in Finance, (Oxford: Oxford University Press).

Shin, Hyun Song, and Kwanho Shin, 2010, “Procyclicality and Monetary Aggregates,” NBER Working Paper w16836. Available via the Internet: www.nber.org/papers/w16836.

Vasicek, Oldrich, 2002, The Distribution of Loan Portfolio Value, Risk, December 2002. Available via the Internet: www.moodyskmv.com/conf04/pdf/papers/dist_loan_port_val.pdf.

Additional information

*Hyun Song Shin is the Hughes-Rogers Professor of Economics at Princeton University. Mundell-Fleming Lecture, presented at the 2011 IMF Annual Research Conference, November 10-11, 2011. The author is grateful to Olivier Blanchard for hosting the lecture. The author also thanks Viral Acharya, James Aitken, Carol Bertaut, Claudio Borio, Michael Chui, Stijn Claessens, Laurie Pounder DeMarco, Pierre-Olivier Gourinchas, Dong He, Haizhou Huang, Ayhan Kose, Ashoka Mody, Goetz von Peter, Philipp Schnabl, Andrew Sheng, Manmohan Singh, and Hui Tong for comments on an earlier draft. The author thanks Daniel Lewis and Linda Zhao for research assistance.

Appendix

Appendix

In this appendix, we present the derivation of the variance of the asset realization w(Y) in Vasicek (2002). Let k=Φ−1(ɛ) and X1, X2,…, X n be i.i.d. standard normal.

where (Z1,…, Z n ) is multivariate standard normal with correlation ρ. Hence

and

where Φ2(·, ·; ρ) cumulative bivariate standard normal with correlation ρ.