Abstract

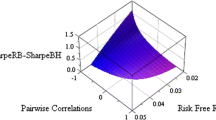

In this article we establish a comparison between the first two moments of the buy-and-hold portfolio and the constantly rebalanced portfolio, under the assumption that the underlying assets follow a geometric Brownian motion. We prove that over a fixed time interval the buy-and-hold portfolio has the greater expected return, with equality if and only if the underlying assets have the same expected returns. We also show that the buy-and-hold portfolio has the larger variance in at least two cases: (i) when the underlying assets have equal expected returns; (ii) when the portfolio weights are mean-variance optimal (unconstrained). These results are easily extended to the case of time varying expected return and volatility. Finally, we consider a numerical comparison of the risk statistics of the two portfolios (standard deviation and value-at-risk) for different portfolio parameters.

Similar content being viewed by others

Notes

Note that to achieve this, the portfolio allocations are constantly changing to reflect the evolving values of the underlying assets.

It follows from Lévy’s theorem, since W t * and (W t *)2−t are both continuous martingales.

The weights add up to one since ∑ i ∑ j w i w j =(∑ i w i )2=1.

This condition is automatically satisfied when C is a diagonal matrix.

For a random variable X, qα(X) is defined by P(X ⩽ qα(X)) = α. For the standard normal, q1%*=−2.326 and q5%*=−1.645.

References

Mulvey, J. and Kim, W.C. (2009) Fixed mix strategy. In: R. Cont (ed.) Encyclopedia of Quantitative Finance, UK: John Wiley and Sons.

Hallerbach, W.G. (2014) Disentangling rebalancing returns. The Journal of Asset Management 15 (Oct): 301–316.

Author information

Authors and Affiliations

Appendix

Appendix

Log normal statistics

Proposition 5.1

-

Assume z i ~ N(μ i , σ i 2) are joint Gaussian random variables with covariance cov(z i , z j )=C ij and variance σ i 2=C ii . If

, then

, then

, then

, then

Proof. The moment generating function of the standard normal Z~ N(0, 1) is  . Hence

. Hence  and

and  . For the covariance, note that

. For the covariance, note that  and z

i

+z

j

~N(μ

i

+μ

j

, σ

i

2+σ

j

2+2C

ij

).

and z

i

+z

j

~N(μ

i

+μ

j

, σ

i

2+σ

j

2+2C

ij

).

□

Corollary 5.2

-

Let z i and

as before, and w

i

scalars. Then

as before, and w

i

scalars. Then

as before, and w

i

scalars. Then

as before, and w

i

scalars. Then

Rights and permissions

About this article

Cite this article

Spinu, F. Buy-and-hold versus constantly rebalanced portfolios: A theoretical comparison. J Asset Manag 16, 79–84 (2015). https://doi.org/10.1057/jam.2015.2

Received:

Revised:

Published:

Issue Date:

DOI: https://doi.org/10.1057/jam.2015.2