Abstract

This article proposes a new empirical methodology for computing a cross-market volatility index – coined CMIX – based on the Factor-Dynamic Conditional Correlation (DCC) model, implemented on volatility surprises. This approach solves problems in treating high-dimensional data and estimating time-varying conditional correlations. We provide an application to multi-asset market data composed of equities, bonds, foreign exchange rates and commodities during 1983–2013. This new methodology may be attractive to asset managers, because it provides a simple way to hedge multi-asset portfolios with derivatives contracts written on the CMIX.

Similar content being viewed by others

Notes

Note that PCA can also be used for the correlation matrix

of

of  .

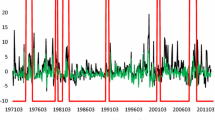

.Figure 4 shows the result of the ABC criterion to determine the number of factors. On the x-axis, the reader can observe that the solid black line ends at 1.5. Hence, the correct number of factors is strictly superior to 1, with the next integer being 2. Note that the dotted line represents the empirical variance of the estimated number of factors.

Note that the factors estimated by PC are only identified up to a non-singular rotation, and therefore do not have a structural economic interpretation.

The AR(1)-GARCH(1, 1) and the DCC(1, 1) models are the baseline specifications in any applied work. For the sake of simplicity, we do not want to artificially increase the number of parameters, which could turn out to be a computational burden in the estimation of the Factor-DCC model.

Basics of portfolio theory can be found in Grinold and Kahn (2000).

We may cite, among others, the study by Dash and Moran (2005) that documented a Sharpe ratio equal to 0.91 for the VIX.

Note that risk-averse investors would certainly prefer to invest in standard stocks/bonds portfolios, instead of volatility indices.

See DeRoon and Nijman (2001) for a survey of mean-variance spanning tests.

of

of  .

.References

Alessi, L., Barigozzi, M. and Capasso, M. (2010) Improved penalization for determining the number of factors in approximate factor models. Statistics and Probability Letters 80 (23–24): 1806–1813.

Alexander, C. (2000) Orthogonal methods for generating large positive semi-definite covariance matrices. University of Reading, UK. ISMA Center Discussion Papers in Finance 2000–06.

Alexander, C. (2001) Market Models: A Guide to Financial Data Analysis. Chichester, UK: Wiley.

Bai, J. and Ng, S. (2002) Determining the number of factors in approximate factor models. Econometrica 70 (1): 191–221.

Baudry, P., Collard, F. and Portier, F. (2011) Gold rush fever in business cycles. Journal of Monetary Economics 58 (2): 84–97.

Boon, L.N. and Ielpo, F. (2012) Determining the Maximum Number of Uncorrelated Strategies in a Global Portfolio. Social Science Research Network: USA. SSRN Working Paper.

Buyuksahin, B. and Harris, J.H. (2011) Do speculators drive crude oil futures prices? Energy Journal 32 (2): 167–202.

Connor, G. and Korajczyk, R.A. (1993) A test for the number of factors in an approximate factor model. Journal of Finance 48 (4): 1263–1291.

Dash, S. and Moran, M.T. (2005) VIX as a companion for hedge fund portfolios. Journal of Alternative Investments 8 (3): 75–80.

DeRoon, F.A. and Nijman, T.E. (2001) Testing for mean-variance spanning: A survey. Journal of Empirical Finance 8 (2): 111–155.

Ding, Z. (1994) Time series analysis of speculative returns. PhD dissertation, University of California, San Diego, USA.

Engle, R. (1993) Technical note: Statistical models for financial volatility. Financial Analysts Journal 49 (1): 72–78.

Engle, R. (2009) Anticipating Correlations: A New Paradigm for Risk Management. USA: Princeton University Press, p. 154.

Goodwin, T.H. (1998) The information ratio. Financial Analysts Journal 54 (4): 34–43.

Grinold, R.C. and Kahn, R.N. (2000) Active Portfolio Management. 2nd edn. New York, USA: MacGraw Hill.

Hallin, M. and Liška, R. (2007) Determining the number of factors in the general dynamic factor model. Journal of the American Statistical Association 102 (478): 603–617.

Hamao, Y., Masulis, R.W. and Ng, V. (1990) Correlations in price changes and volatility across international stock markets. Review of Financial Studies 3 (2): 281–307.

Huberman, G. and Kandel, S. (1995) Mean-variance spanning. Journal of Finance 42 (4): 873–888.

Kan, R. and Zhou, G. (2012) Tests of mean-variance spanning. Annals of Economics and Finance 13 (1): 139–187.

Hood, M. and Malik, F. (2013) Is gold the best hedge and a safe haven under changing stock market volatility? Review of Financial Economics 22 (2): 47–52.

Mensi, W., Beljid, M., Boubaker, A. and Managi, S. (2013) Correlations and volatility spillovers across commodity and stock markets: Linking energies, food and gold. Economic Modelling 32: 15–22.

Onatski, A. (2009) Testing hypotheses about the number of factors in large factor models. Econometrica 77 (5): 1447–1479.

Sharpe, W.F. (1966) Mutual fund performance. Journal of Business 39 (1): 119–138.

Stock, J. and Watson, M. (2002a) Forecasting using principal components from a large number of predictor. Journal of the American Statistical Association 97 (460): 1167–1179.

Stock, J. and Watson, M. (2002b) Macroeconomic forecasting using diffusion indexes. Journal of Business and Economic Statistics 20 (2): 147–162.

Stock, J. and Watson, M. (2005) Implications of Dynamic Factor Models for VAR Analysis. NBER Working Paper no. 11467, National Bureau of Economic Research, Massachusetts, USA.

Stock, J. and Watson, M. (2006) Forecasting using many predictors. In: G. Elliott, C. Granger and T. Timmerman (eds.) Handbook of Economic Forecasting 1. North Holland: pp. 515–554.

Switzer, L. and Fan, H. (2007) Spanning tests for replicable small-cap indexes as separate asset classes. Journal of Portfolio Management 33 (4): 102–110.

Tsay, R.S. (2010) Analysis of Financial Time Series. 3rd edn. New York, USA: John Wiley and Sons.

Zhang, K. and Chan, L. (2009) Efficient factor GARCH models and Factor-DCC models. Quantitative Finance 9 (1): 71–91.

Author information

Authors and Affiliations

Corresponding author

Appendix

Appendix

Number of factors based on the criterion by Alessi, Barigozzi and Capasso (ABC, 2009). Note: r c;N *T is the number of factors pointed out by the Alessi et al (2010) criterion with T the time and N the cross-section dimensions of the dataset. S c is the empirical variance of the estimated number of factors (see Alessi et al (2010) for more details). c is an arbitrary positive real number. The test statistics use the two information criteria:

with V the residual variance of the idiosyncratic components (see Bai and Ng (2002) for more details) and k common factors. The estimated number of factors is a function of c and, depending on the chosen criterion, is given by:

Rights and permissions

About this article

Cite this article

Aboura, S., Chevallier, J. The cross-market index for volatility surprise. J Asset Manag 15, 7–23 (2014). https://doi.org/10.1057/jam.2014.5

Received:

Revised:

Published:

Issue Date:

DOI: https://doi.org/10.1057/jam.2014.5