Abstract

This article presents a tractable and empirically sound technique for generating stressed probabilities of default (PDs), which are then used to derive loss rates for the provisioning of a bank's risk-based capital. This work is in response to the recent regulatory findings attributed to the Supervisory Capital Assessment Program (SCAP) stress tests of 2009, which revealed weaknesses in the existing regulatory and economic capital approaches. The SCAP projected losses of approximately US$82.4 billion in banks’ credit card portfolios for 2010, highlighting the need for better forecasting and stress testing of revolving retail exposures. This study proposes a timely model that will improve the ability of banks to determine the capital adequacy of revolving retail exposures. Using options theory, we discuss why an obligor may default and produce estimates of expected losses from our stressed PDs so as to determine loss provisions. This method relies on the simulation of PD distributions via changes in selected macroeconomic variables and the cardholder's debt-to-income ratio. The methodology offers the flexibility of being tractable and scalable to data in the issuer's credit card portfolio by geography and credit quality of the obligor.

Similar content being viewed by others

Notes

A discussion of the Vasicek loss distribution follows and can also be found in Vasicek2.

To assess the capital positions of the largest US banking organizations, the federal supervisory agencies carried out the SCAP stress tests in the spring of 2009 (see Board of Governors4).

The BIS Committee on the Global Financial System (BCGFS) (2009) defines ‘Stress testing’ as – ‘the techniques used by financial firms to gauge their potential vulnerability to exceptional but plausible events’.

Under the Basel II requirement, a higher level of confidence (such as 99.99 per cent) is necessary to compute the required capital amount (see Hugh and Wang57 for more interpretations).

There are two types of DTIRs that lenders compute when households seek credit, These are (i) The front-end ratio, also called the housing ratio, shows the percentage of an obligor's income that goes toward housing expenses, including monthly mortgage payments, real estate taxes, homeowner's insurance and association dues; (ii) The back-end ratio shows the portion of an obligor's income is needed to cover all monthly debt obligations. This includes credit card bills, car loans, child support, student loans and any other debt that shows on the credit report, plus mortgage and other housing expenses. Lenders typically say the ideal front-end ratio should be no more than 28 per cent, and a back-end ratio not exceeding 36 per cent..

Several large banks follow the IRB approach required by the Basel Capital Accord for determining expected loss rates. Although some inputs to the IRB approach such as the LGD and EAD maybe directly observable from the historical data, the PD is usually not, and needs to be estimated. The accuracy with which this is done can have significant effects on loss rates calculations.

Such models that are used to determine whether an applicant should be granted credit are based on data collected at the time of application that then remain fixed. Typically, this is information taken from a completed application form and a credit score for the individual provided by a credit bureau.

Note that the customer's option to default for cash flow or leverage reasons is distinctly a non-linear relationship. These relationships are handled in a probabilistic manner, which captures the economic idea that after a certain threshold level, a customer's payment practices will become very sensitive to macroeconomic shocks.

This is consistent with Merton43 who suggests that a borrower defaults when the value of his assets falls below a certain threshold level.

We use the narrower definition of household assets; income, because based on the available Federal Reserve data, US households’ savings rate was less than 2 per cent of disposable income for several years and the available assets needed by the median family to insulate a loss of labor income was very small (well below the advisable 6 months of savings).

The aggregate debt-to-income data of the Federal Reserve is not reflective of the household budgetary realities of the median family. Plus it does not allow for segmentation by geographic region.

Because the national credit bureaus do not maintain real-time data on obligors’ incomes similar to the extensive data on debt service commitments, researchers are forced to find representative proxies for household's income.

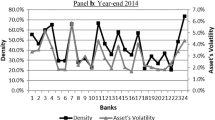

Here segmented may be considered in terms of the bank's geographic distribution of credit card issuance or it could be in terms of the credit quality of the cardholders. Banks typically categorize credit cardholders based on credit riskiness into one of several internally determined credit categories.

The dynamic version suggests that both past and current output can impact the current level of unemployment. In the difference version of Okun's law, this implies that some relevant variables have been omitted from the right side of the equation. Second, including past changes in the unemployment rate as variables on the right side eliminates serial correlation in the error terms.

As discussed earlier, the credit card portfolio maybe segmented in terms of the bank's geographic distribution of credit card issuance or in terms of the credit quality of the cardholders. Banks typically categorize credit cardholders based on credit riskiness into one of several credit categories.

References

Vasicek, O. (1987) Probability of loss on loan portfolio. KMV Corporation http://kmv.com.

Board of Governors of the Federal Reserve System (FRS). (2009) The Supervisory Assessment Program: Overview of Results. Washington, DC: Board of Governors. White paper, http://www.federalreserve.gov/newsevents/press/bcreg/bcreg20090507a1.pdf.

Sorge, M. (2004) Stress-Testing Financial Systems: An Overview of Current Methodologies. BIS Working Papers, No. 165.

Froyland, E. and Larsen, K. (2002) How vulnerable are financial institutions to macroeconomic changes? An analysis based on stress testing. Economic Bulletin, Norges Bank.

Hoggarth, G. and Whitley, J. (2003) Assessing the strength of UK banks through macroeconomic stress tests. Financial Stability Review, Bank of England.

Mawdsley, A., McGuire, M. and O'Donnell, N. (2004) The Stress Testing of Irish Credit Institutions. Financial Stability Report, Central Bank and Financial Services Authority of Ireland.

Bunn, P., Cunningham, A. and Drehmann, M. (2005) Stress testing as a tool for assessing systemic risks. Financial Stability Review, Bank of England, June.

Basel Committee on Banking Supervision (BCBS). (2009) Principles for Sound Stress Testing Practices and Supervision – Final Paper. Working Report from Committee on the Global Financial System.

Basel Committee on Banking Supervision (BCBS). (2010) Basel II: The Basel Committee's response to the financial crisis: Report to the G20, http://www.bis.org/list/bcbs/page_1.htm.

Miele, M. and Sales, E. (2011) The financial crisis and regulation reform. Journal of Banking Regulation 12 (4): 277–307.

Calem, P. and LaCour-Little, M. (2001) Risk-based capital requirements for mortgage loans. Journal of Banking and Finance 28 (3): 647–672.

Black, S.E. and Morgan, D.P. (1998) Risk and the Democratization of Credit Cards. Federal Reserve Bank of New York. Research Paper 9815.

Bridges, S. and Disney, R. (2001) Modeling Consumer Credit and Default: The Research Agenda. Experian Centre for Economic Modeling Working Paper.

Crook, J. and Bellotti, T. (2009) Asset Correlations for Credit Card Defaults. Credit Research Centre, University of Edinburgh Business School Working Paper.

Crook, J. and Bellotti, T. (2009) Time varying and dynamic models for default risk in consumer loans. Journal of the Royal Statistical Society Series A (Statistics in Society) 173 (2): 279–468.

Crook, J. and Banasik, J. (2005) Does reject inference really improve the performance of application scoring models. Journal of Banking and Finance 24 (4): 857–874.

Boss, M. (2002) A Macroeconomic Credit Risk Model for Stress Testing the Austrian Credit Portfolio. Oesterreichische National Bank. Financial Stability Report 4.

Gasha, J.G. and Morales, R. (2004) Identifying Threshold Effects in Credit Risk Stress Testing. IMF Working Paper No. WP/04/150.

Virolainen, K. (2004) Macro Stress-Testing with a Macroeconomic Credit Risk Model for Finland. Bank of Finland Discussion Paper, No. 18/2004.

Whitley, J., Windram, R. and Cox, P. (2004) An Empirical Model of Household Arrears. Bank of England Working Paper No. 214.

Crook, J. and Bellotti, T. (2010) Time varying and dynamic models for default risk in consumer loans. Journal of the Royal Statistical Society Series A (Statistics in Society) 173 (2): 279–468.

Thomas, L.C., Ho, J. and Scherer, W.T. (2001) Time will tell: Behavioral scoring and the dynamics of consumer credit assessment. IMA Journal of Management Mathematics 12: 89–103.

Bellotti, T. and Crook, J. (2009) Credit scoring with macroeconomic variables using survival analyses. The Journal of the Operational Research Society 60 (12): 1699–1707.

Breedon, J., Thomas, L. and McDonald III, J. (2008) Stress testing retail loan portfolios with dual-time dynamics. The Journal of Risk Model Validation 2 (2): 43–62.

Breeden, J.L. and Ingram, D. (2009) The relationship between default and economic cycles across countries for retail portfolios. Journal of Risk Model Validation 2 (3): 11–44.

Rösch, D. and Scheule, T. (2004) Forecasting retail portfolio credit risk. Journal of Risk Finance 5 (2): 16–32.

Gross, D.B. and Souleles, N.S. (2002) An empirical analysis of personal bankruptcy and delinquency. The Review of Financial Studies 15 (1): 319–347.

Calhoun, C.A. and Deng, Y. (2002) A dynamic analysis of fixed- and adjustable-rate mortgage terminations. Journal of Real Estate Finance and Economics 24 (1): 9–33.

Gerardi, K., Shapiro, A.H. and Willen, P.S. (2008) Subprime Outcomes: Risky Mortgages, Homeownership Experiences, and Foreclosures. Federal Reserve Bank of Boston Working Paper 07–15.

Wilson, T.C. (1997a) Portfolio credit risk (I). Risk 10 (9): 111–117.

Wilson, T.C. (1997b) Portfolio credit risk (II). Risk 10 (10): 56–61.

Wong, J., Choi, K.F. and Fong, T. (2006) A framework for stress testing banks’ credit risk. HKMA Research Memorandum, 15.

Merton, R. (1974) On the pricing of corporate debt: The risk structure of interest rates. The Journal of Finance 29 (2): 449–470.

Finger, C. (1998) Sticks and Stones. Risk Metrics Group. Working Paper.

Gordy, M.B. and Heitfeld, N. (2000) Estimating Factor Loading When Rating Performance Data Are Scarce. Board of Governors of the Federal Reserve System, Division of Research and Statistics. Working paper.

Gordy, M. and Heitfield, E. (2002) Estimating Default Correlations from Short Panels of Credit Rating Performance Data. Federal Reserve Board Working Paper.

Okun, A.M. (1962) Potential GNP: Its measurement and Significance. In: Proceedings of the Business and Economic Statistics Section, Washington DC: American Statistical Association, pp. 98–103.

Knotek II, E. (2007) How useful is Okun's law. Economic Review, Kanasas City Federal Reserve Bank, 4th Quarter.

Basel Committee on Banking Supervision (BCBS). (2006) International convergence of capital measurement and capital standards: A revised framework comprehensive version. Bank of International Settlements, June.

Hugh, T. and Wang, Z. (2005) Interpreting the internal ratings-based capital requirements in Basel II. Journal of Banking Regulation 6 (3): 274–289.

Author information

Authors and Affiliations

Corresponding author

Appendices

Appendix A

THE LOGIT TRANSFORMATION

The first step in defining the model for our data concerns the systematic structure, where the probabilities λ i depend on the vector of observed covariates z i in equation (6). The simplest idea would be to let λ it be a linear function of the covariates, say

where β is a vector of sensitivities discussed in equation (6). Equation (A.1) is sometimes called the linear probability model. This model is often estimated from individual data using ordinary least squares (OLS). One problem with this model is that the probability λ it on the left-hand side has to be between 0 and 1, but the linear predictor z it β on the right-hand side can take any real value, and thus there is no guarantee that the predicted values will be in the correct range unless complex restrictions are imposed on the coefficients. A simple solution to this problem is to transform the probability to remove the range restrictions, and model the transformation as a linear function of the covariates. We do this in two steps.

First, we move from the probability λ it to the odds

defined as the ratio of the probability to its complement, or the ratio of favorable to unfavorable cases.

Second, we take logarithms, calculating the logit or log-odds

which has the effect of removing the floor restriction. To see this point, note that as the probability goes down to 0 the odds approach 0 and the logit approaches −∞. At the other extreme, as the probability approaches one, the odds approach +∞ and so does the logit.

The logit transformation is one to one. The inverse transformation is sometimes called the anti-logit, and allows us to go back from logits to probabilities. Solving for λ it in equation (A.3) gives

Appendix B

The credit card portfolio accross an issuer's various credit classes or geograhic locations can be aggregated into one overall loss distribution. To accomplish this, we begin by define equation (1) for each exposure class l(l=1,2, …3) and each asset return as R it l:

where

(i=1, …, N t .t=1, …, T) are normally distributed with mean (θ) 0 and standard deviation (σ) 1. Idiosyncratic shocks U it are assumed to be independent from the systematic factor F t and independent for different borrowers. All random variables are serially independent.

The correlation between any two asset returns is then as follows:

where

Denotes the correlation between the random factors of two different credit classes. Using these correlation estimates, the loss distributions can be calculated by integrating over the joint distribution of the random effects. Although the one-dimentional integral from section ‘The analytical model’ was numerically tractable, in general a higher dimentional integral requires a bit more sohistication, which can be acheived using Monte Carlo simulations.

Rights and permissions

About this article

Cite this article

Dunbar, K. Forecasting and stress testing the risk-based capital requirements for revolving retail exposures. J Bank Regul 13, 249–263 (2012). https://doi.org/10.1057/jbr.2012.5

Published:

Issue Date:

DOI: https://doi.org/10.1057/jbr.2012.5