Abstract

This paper investigates the effect of resource nationalism on the value of petroleum (crude oil and natural gas) reserves. We develop a framework for treating resource nationalism as political risk, and utilize data on reserve transactions (from John S. Herold) and political risk ratings (from International Country Risk Guide and Institutional Investor) for the period 2000–2006. Controlling for other factors that affect reserve value, we demonstrate the value destruction of political risk, and estimate the political risk discount for 37 countries. The paper contributes to both the international business literature and practitioner approaches to political risk analysis in demonstrating use of publicly available market data from real-asset transactions to measure the cost of political risk. We also show that the discount depends on market conditions: the higher expected future petroleum prices are, the larger is the discount at any level of political risk. This insight adds a new dimension to analysis of political risk, which is typically measured and examined without regard to market conditions.

Similar content being viewed by others

INTRODUCTION

The big theme of the oil and gas business in 2006 was resource nationalism … host countries find that oil market forces have shifted in their favor, enabling them to advance their interests much more effectively. (Petroleum Intelligence Weekly, 2007a)

International oil companies can invoke the sanctity of contracts and may even prevail in arbitration, but they risk losing access to resources if they upset their hosts. (Petroleum Intelligence Weekly, 2007b)

During the past few years, energy issues have grabbed international headlines, particularly regarding the resource nationalism of petroleum-exporting countries. A sampling of events from 2006 is illustrative. Bolivia nationalized its oil and gas industry in May, raising the profile of resource nationalism considerably. Ecuador used troops to take over Occidental Petroleum's holdings in the same month, and then turned them over to state-owned Petroecuador. In August, Chad created a national oil company, and expelled Chevron and Petronas, two of the largest foreign oil investors.Footnote 1 In September, Russia forced contract renegotiations that eventually pressed BP and Shell into turning over majority stakes in their petroleum operations to local state-owned enterprises. In December, Venezuela mandated the sale of foreign-owned assets, eventually forcing Exxon and ConocoPhillips to leave the country, although BP and Statoil remained with minority partnerships. Lower-profile intervention occurred in other countries, and interventions have continued in subsequent years.

“Resource nationalism” broadly refers to state control or dominance of natural resources, and the resulting potential to use this power for political and economic purposes, including relationships with foreign investors. At the heart of resource nationalism is a government's intervention in its country's natural resource industries to protect or enhance its national patrimony and sovereignty. Such intervention may include nationalization, forced partnerships, tax increases, expanding regulation, etc.

The small scholarly literature on resource nationalism is descriptive (Brunet & Lentini, 2007; Stevens, 2008; Wälde, 2008). We provide an analytical perspective, viewing the phenomenon through the lens of political risk, a central topic in international business (Kobrin, 1979). Concern over political risk in natural resource industries has a long history in international business, dating back to the obsolescing-bargain theory developed by Vernon (1971), who applied it first to raw materials. Earlier, Barlow and Wender (1955) found that multinational enterprise (MNE) managers in extractive industries were far more concerned about host-government policies than were those in manufacturing.Footnote 2

Although news coverage of resource nationalism and the existing literature on political risk are extensive, they almost never consider the market implications of intervention. The market may exact a price for resource nationalism – the value of the very resources on which natural-resource-rich countries depend may be damaged as a consequence of government intervention. Surprisingly, the destruction of market value from resource nationalism has not been examined in the literature. To help fill the void, this paper analyzes the phenomenon in the petroleum industry, specifically considering how political risk affects the valuation of oil and gas reserves. Thus the paper investigates what happens when resource nationalism meets the market.

Petroleum is a global industry, and accounts for the largest single component of international trade (Weiner, 2005). Several factors make the industry fertile ground for investigating political risk. First, political risk is probably more important in this industry than in any other. Indeed, natural resource industries, of which petroleum is by far the largest, have accounted for the greatest number of expropriations of foreign direct investment (FDI) (Kobrin, 1980, 1984a, 1984b, 1985). Early nationalizations of foreign multinationals took place in the petroleum industry in Bolivia and Mexico in the 1930s. This is in part due to the large rent component in natural resource prices, and in part due to beliefs that natural resources are a country's national patrimony. Indeed, some countries (e.g., Mexico, Saudi Arabia) do not allow any FDI in developing their petroleum resources.

Second, petroleum is one of the largest industries for cross-border investment. Notwithstanding past nationalizations, multinationals have long accounted for much of the investment in the industry. This is partially a result of geology – petroleum reserves are scattered across the globe, many in nations lacking well-developed legal and security systems. Resource nationalism is typically associated with actions against FDI.

Third, many countries are dependent on petroleum for a substantial part of their economies, exports, and fiscal revenues. Government intervention in the industry is widespread, and hence so is the opportunity for wrestling over rents with MNEs (Vernon, 1971).Footnote 3 Moreover, high economic stakes and weak property rights fuel rent-seeking by private groups through bribery or armed conflict. According to the World Bank (Bannon & Collier, 2003), natural resource abundance exacerbates the risk of violent conflict. Civil conflict has exacerbated political risk in oil countries such as Angola, Chad, Indonesia, and Nigeria.

Finally, competition in a world market for a predominantly homogeneous product facilitates measurement of the effects of intervention. The sheer size of the industry has generated intense scrutiny, and extensive data collection. Quantitative data have become more important to political risk research as scholarship has moved from more subjective and descriptive measures to statistical analysis (see, e.g., Click, 2005).

We are able to contribute to the body of literature examining political risk in natural-resource industries by exploiting a database of petroleum reserve transactions to empirically measure the consequences of intervention. We focus our attention on prices of petroleum reserves because value is clearly tied to the jurisdictional location of the asset. The value of the output is similar across locations, as oil and natural gas are largely homogeneous commodities. Hence the value of the reserves will vary across locations primarily because of differences in the costs for extracting them and differences in jurisdictional treatment. We are able to control for extraction cost differences: hence any differences associated with political jurisdictions must be associated with political risk.

Our idea is very simple. Suppose two countries have reserves of a natural resource such as petroleum. Once extracted, the output of the two countries is indistinguishable – all output sells for the same price in a global market. When reserves in the two countries are valued (perhaps in dollars per unit of reserve, such as barrel of oil), the value will depend on the world price of the output, but this price will not affect valuation of reserves in the two countries differently. Extraction costs may differ, however, and these costs will affect the valuation of reserves differently because the higher-cost location will have lower valuations than the lower-cost location.

We hypothesize that host-country political risk acts like an additional cost: all other things equal, the jurisdiction with higher political risk will experience lower valuations than the jurisdiction with lower political risk. We refer to the lower valuation in percentage terms as a political risk discount. Measuring political risk is in general a subjective exercise; one of our main goals in this paper is to demonstrate use of market data to construct an objective discount measure of political risk.

This paper draws on a dataset of transactions in which reserves of oil and gas located in different national jurisdictions are traded. The market value of each exchange is known, and we investigate the determinants of value in order to ascertain whether the risk characteristics of the location are important. The investigation allows us to calculate the amount by which the asset is discounted for resource nationalism.

A major challenge in studying resource nationalism is that it is difficult to quantify. However, several analysts produce ratings of political risk by country through time. (For a survey see Howell, 2006.) We use the political risk index disseminated by the International Country Risk Guide (ICRG) and the sovereign risk index published in Institutional Investor magazine as quantitative proxies for resource nationalism. Strictly speaking, the Institutional Investor rating is not a measure of political risk, but a specific dimension – a country's creditworthiness in international markets. We use it as a proxy for political risk, and note that it is in fact highly correlated with the ICRG rating (the correlation coefficient is 0.85 in our sample). Since most political, sovereign, and country ratings are positively correlated, we consider these two measures as broadly representative of the indices available. It is worth noting, however, that the ratings are general host-country risk ratings, and do not pertain exclusively to the risks in the petroleum sector.

We employ these risk ratings as determinants of the value of petroleum (i.e., oil and gas) reserves in regressions controlling for oil and gas prices, the type of reserve, and the mix of oil and gas. Our results demonstrate that the value of reserves per barrel of oil equivalent (boe) are sensitive to nations’ scores on these risk ratings. We are thus able to calculate an asset discount for the 37 countries in our sample relative to the US. For example, reserves in Russia trade at a 58% discount using the ICRG index (or a 74% discount using Institutional Investor) compared with what they would fetch if they were in the US. The magnitude of these discounts is quite large, supporting and quantifying intuition that political risk is a major consideration for investors and host governments.

Moreover, we find evidence that the political-risk discount depends on the prices of oil and gas, such that the discount is low when the price of oil/gas is low, and high when the price is high. Using the ICRG data, we consider historically low and high prices of $25 and $40 per barrel, respectively. If the price of oil is $25 per barrel, the discount on reserves in Russia is 52%. However, when the price of oil is $40 per barrel, the discount on reserves in Russia rises to 88%. The finding that the discount for political risk depends on the prices of oil and gas is an important insight, because most ratings are constructed without regard to market conditions; see, for example, Cosset and Roy (1991).

The main contribution of this paper is quantification of the cost of resource nationalism by estimating the discount on the value of petroleum reserves associated with the country in which the reserves are located. This successfully prices political risk in natural resource industries more generally. The research therefore answers questions that are of interest to MNEs managing existing foreign investments or considering new investment abroad in natural resource industries; to investors and analysts who follow MNE securities; and to government policymakers in resource-rich countries who seek to influence the level of investment.

A second contribution of this paper is the careful consideration of the link between political risk and market risk. The existing literature tends to treat political risk and market risk separately, but the quotes at the opening of this introduction suggest that, in practice, politics and markets may be closely related. Volatile prices may exacerbate political risk during booms and mitigate it during busts. We demonstrate how to address such interaction, and implement statistical tests to determine whether it is significant in the petroleum industry. Our findings indicate that it is, suggesting that treating political risk and market risk separately in valuation of petroleum reserves is likely to yield inaccurate estimates of asset value. To our knowledge, this is one of the first papers in the literatures on political risk and international business to document this interaction effect.

A third contribution of this paper is strengthening of the political risk and international business literatures. While scholars tend to write about the costs of political risk conceptually, this paper approaches the question empirically. The research is noteworthy because, to our knowledge, there has not been a serious attempt to measure the cost of political risk using market prices of assets. Analysis of prices has been limited to interest-rate premia on bonds – such as sovereign bonds – or aggregate market returns on stocks. However, bond valuation involves an assessment of the riskiness of the borrower rather than the riskiness of the asset location. Several studies suggest that stock returns are higher in countries with more political risk and within a country during periods with more risk, but these do not directly consider the pricing of assets and cannot arrive at an estimate of an asset discount.

EMPIRICAL CONTEXT: PETROLEUM RESERVES

Political risk focuses on real investments (operations abroad), which are difficult to value; unlike financial assets, market prices are not readily available. Difficulty in valuing investment hinders research on impacts of political risk. In the case of the global petroleum industry, however, two factors allow us to overcome this limitation. The first is asset homogeneity: unlike manufacturing, where value cannot easily be compared across plants, petroleum assets produce similar products everywhere. Such asset heterogeneity as exists can be largely controlled for through the use of proxies for production cost. The second factor is a liquid market for trade in assets and data on such trades, which allows researchers to observe value directly.

The very fact that asset location decisions are exogenous (determined through geology, not managerial decision-making) serves both to eliminate self-selection/simultaneity bias in empirical analysis, and to allow examination of a much wider set of nations than is ordinarily possible in studies of international investment. Our data include host countries that ordinarily would be problematic for examining investment, including sub-Saharan countries such as Namibia and Sudan, Middle Eastern countries such as Oman and Syria, and Asian countries such as Indonesia and Papua New Guinea, in addition to a geographically and industrially diverse group of countries more commonly included in studies of FDI.

The assets traded are petroleum reserves, that is, oil and gas in the ground. The exact size of a reserve is unobservable by market participants; instead, a probabilistic definition is employed. Oil and gas reserves are typically characterized as proved (1P) or proved+probable (2P). Proved reserves refers to the quantity of oil and gas in the ground that is extractable economically at current prices and costs with 90% probability. Probable reserves are similarly defined, but with 50% probability. In this paper, we use transactions relating to 1P, so there is a fair amount of certainty about the size of the reserve at the time of the trade, and the transaction value reflects this certainty. Reserves are the capital base of the firm, and serve as collateral for loans. As a result, considerable care is taken in estimating their size, typically by independent consulting firms specializing in reserve audits, which are based on engineering, petroleum geology, and experience. The auditing process provides a measure of integrity, and gives us confidence in the use of data for research. Reserves are sufficiently important to firm value that announcements of reserve restatements typically are associated with abnormal stock returns.Footnote 4

Reserves are traded in three primary ways. Mergers entail purchase of an entire firm, including its assets and liabilities. Acquisitions are like mergers, but entail purchase of only a fraction of the target firm's equity. Asset sales refer to specific geological assets, and entail no claim on the seller's equity. All three ways are included in the database, but asset sales predominate. Such sales are typically smaller in size and value than mergers and acquisitions, although there are exceptions. For example, two of the largest transactions in 2006 were Norsk Hydro's sale of its oil and gas operations to Statoil for about $29 billion, and Gazprom's purchase of a 50% share of the Sakhalin II consortium from Royal Dutch Shell, Mitsui, and Mitsubishi for about $7.5 billion.Footnote 5

How much is oil and gas in the ground (reserves) worth? Does political risk influence these values? If so, how much of a discount should be applied with increasing political risk? We take up these questions in this paper. The statistical analysis below can be foreshadowed by a simple graph of the value of petroleum reserves against expected future petroleum prices. Figure 1 shows that a linear relationship between the log of asset value and the log of expected petroleum price is likely to fit well, but that there is a great deal of dispersion in reserve values. How much of the reserve discount (or premium) is due to political risk? Figure 1 suggests this visually by highlighting the three non-North American countries with the most deals – Indonesia, Russia, and the United Kingdom. The first two of these tend to be rated as high political risk. A substantial political risk discount can be inferred from the graph, since the observations for Indonesia and Russia appear to be regularly below the observations for deals in general, and UK deals in particular.

Reserve values (Herold M&A deals) vs expected petroleum prices (oil and gas futures strip), 2000–2006 Q3.

THEORY AND HYPOTHESES

The scholarly literature focuses primarily on the effects of political risk on decisions regarding FDI and cross-border capital flows.Footnote 6 Surprisingly absent from the literature is discussion or analysis of market impacts: to what extent does political risk affect the value of investment? Most FDI is through mergers and acquisitions (M&A); cross-border M&A accounted for between 82% and 89% of FDI in 2007, depending on the FDI measure used (United Nations, 2008: 10). Managers evaluating investment opportunities for international expansion need to factor in political risk in valuing potential target assets. While consultancies provide subjective assessments of political risk, market-based discounts have the advantage of incorporating the views of market participants risking their own capital, and offer an alternative to the subjective measures now in use.

While this paper is the first to examine the relationship between measures of political risk and the market value of real assets, there is a small literature on sovereign risk and financial assets, and sovereign debt in particular. The theory is straightforward: the greater the likelihood that sovereign borrowers are unable or unwilling to repay their debt, the riskier are their sovereign bonds, and thus the greater is the interest rate spread on their sovereign bonds over the risk-free rate. Empirical studies include Block and Vaaler (2004), Boubakri, Cosset, and Smaoui (2009), and Vaaler, Schrage, and Block (2005). Several authors have studied the effect of political risk on currency markets (Cosset & Rianderie, 1985) and stock markets (Bailey & Chung, 1995; Beaulieu, Cosset, & Essaddam, 2005, 2006; Bilson, Brailsford, & Hooper, 2002; Diamonte, Liew, & Stevens, 1996; Erb, Harvey, & Viskanta, 1996; Phillips-Patrick, 1989).

Political risk exposure may differ substantially between real and financial assets, however. Policy changes affect future cash flows associated with financial assets, whereas in the case of real investment the asset itself is exposed. The influence of political risk on the value of real assets should be of particular relevance to companies engaged in FDI, as well as to international business scholars.

Petroleum reserves have not been used to examine political risk, but researchers have used the reserves market to test the leading theory of resource pricing (Hotelling, 1931), which predicts that the net price (price of the resource once extracted, less extraction cost) of a natural resource in the ground will rise over time at the interest rate as the resource is depleted.Footnote 7 The reserves market has also been used to study merger activity: for example, Ghicas and Pastena (1989) examine cash flows associated with reserves reported in firms’ 10-K filings as predictors of values in 44 US petroleum mergers.

The literature review above suggests the need for an asset pricing model in order to establish a benchmark for asset values in the absence of political risk. Our model is designed to be as simple as possible. The value of a petroleum reserve is given by

where VR refers to reserve value, R is the size of the reserve, and PE and CE are respectively expected petroleum prices and costs over the life of the reserve. We have data on VR and R, and can easily obtain proxies for PE. Adelman and Watkins (2005) note that cost data are generally unavailable, and subsequently assume that cost is 35% of price. In practice, costs are often taken as proportional to prices:

both because the main component of costs is output taxes, and because production costs tend to rise with prices. Since we face the same data constraint on cost data, we carefully interpret the effects of expected prices in light of the absence of cost data. In addition, however, we adjust for costs of non-conventional reserves using simple dummy variables (described further below).

Substituting Eq. (2) into Eq. (1) and dividing by R, we obtain a specification for conventional reserves:

Rewriting in logarithmic form, and introducing political risk variables, additional cost proxies, and control variables, we arrive at the equation we estimate:

We use the value of reserves in the ground on a per-barrel basis, VR/R, as the dependent variable. This is standard in the literature using accounting data to value petroleum companies, and helps reduce heteroskedasticity problems associated with orders-of-magnitude variation in reserve sizes.Footnote 8 We model VR/R as depending on the expected petroleum price PE, political risk, proxies for relative extraction cost, and other control variables. μ is the constant in the equation, and ɛ is the error term.

The value of petroleum in the ground should depend on its market price once extracted, and in Eq. (4) we would expect α>0. If a 1% increase in market price leads to a 1% rise in reserve value, then α=1. Proxies for the market price should reflect expectations of future spot prices prevailing at the time of the transaction. Expectations are unobservable; we use futures prices for crude oil and natural gas as our main measure of expected petroleum prices. In order to be a good proxy for price expectations, crude oil and natural gas futures prices should be unbiased predictors of future spot prices. Chinn, LeBlanc, and Coibion (2005) find unbiasedness for 1-year contract maturities, but longer maturities have not been tested.

The value of a petroleum reserve depends on the nature of the reserve and the cost of extraction. Costs are partially reflected in the constant; if our simplest model of conventional reserves in Eq. (3) is perfect, then μ=ln(1−φ). However, we control for extraction cost differences through use of dummy variables for the technology employed to recover and process the petroleum to get it to market. Our categories include: onshore conventional (the omitted dummy); offshore deep water; offshore shallow water; liquefied natural gas (LNG); coalbed methane; other unconventional gas; synthetic crude oil from tarsands; frontier and enhanced recovery production; diversified; and royalty interest. All of these technologies but the last two are costlier than conventional petroleum extraction, and should decrease the value of the reserve (such that γ i <0). Diversified refers to packages of reserves with diverse characteristics; its effect on reserve value is unclear. Royalty interest is an entitlement to petroleum from the reserve without paying extraction cost, and should increase the reserve value (γROYALTY INTEREST>0).Footnote 9

We also consider three control variables. First, we include a dummy variable for heavy crude because it fetches less in world markets than other types of oil; we thus expect δHEAVY CRUDE <0. Second, we consider the proportion of the reserve in the form of natural gas, rather than oil. This issue is discussed further in the presentation of data below. Third, we consider the source of the transaction information: buyer or seller. Despite the fact that reserves are typically assessed by outside consultants, buyers may be systematically more optimistic in interpreting reserve data and advice than sellers, and report larger reserves. If this is the case, then VR/R will be systematically lower for buyer-reported than for seller-reported transactions; we expect δBUYER REPORT < 0.

DATA

Reserve deals are typically announced by transactors and reported in the trade and business press. Transaction data are compiled by consulting firms, investment banks, and the trade press. The transaction data we use are collected and maintained by the US firm John S. Herold Incorporated (JSH); a subset (those of at least $50 million) is published each year in Petroleum Intelligence Weekly, a leading trade publication. There are many smaller deals, which we obtained from JSH.Footnote 10

The reserve value VR is calculated by subtracting from the reported total market value of the transaction, V, the value of non-reserve assets included in the deal. Such assets typically include undeveloped acreage, processing plants, etc., which JSH subtracts based on book values or market values, according to asset type and data availability. Merger transactions typically also include cash, debt and other liabilities. On average, the value of non-reserve assets is modest, roughly 10% of transaction value. However, because VR is imputed based on accounting data, we also examine the market figure, total transaction value per unit of reserves (denoted V/R), as a dependent variable.

Our sample covers the period 2000 through 2006 Q3, for which JSH reported 1793 reserve deals of at least $10 million, of which 1056 were for at least $50 million, 741 were for at least $100 million, and 123 for at least $1000 million. For each deal, we obtained the announcement date, transaction value, reserve value, reserve size, location, technology/cost proxies (e.g., whether the reserves were offshore, etc.), and whether the deal was reported by the buyer or the seller. The sample includes 1657 of the 1793 deals valued at $10 million or more.Footnote 11 Excluded are deals that did not close (typically offers that were refused by sellers), equity purchases through stock markets, and volumetric production payments, a means of renting reserves for a limited time. Because some variables are missing for some transactions, our final sample consists of 1020 observations. Table 1 presents summary statistics and correlations.

Reserves include both crude oil and natural gas, which are often found together, and are measured in boe. The energy in 1 barrel (bbl) of oil and 6000 cubic feet (mcf) of gas are equal on average, although figures vary some across reserves. We follow the literature in aggregating oil and gas on a thermal-equivalent basis: R=RO+RG/6, where RO and RG are oil and gas reserves, measured in bbl and mcf respectively (Berry, Hasan, & O’Bryan, 1998). As pointed out by Adelman and Watkins (2005), however, the ratio of the market values of oil and gas need not be equal to their thermal ratios. We thus take this into account by obtaining the decomposition of reserves into oil and gas from the JSH database and constructing a variable representing the percentage of natural gas in the total reserve, percent gas=RG/6R. If oil and gas are identically priced, based on their energy equivalent, the coefficient on the percentage of gas in the reserves will be zero: δGAS PERCENT=0.

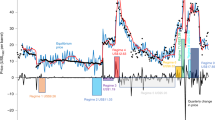

We matched the JSH data with two other types of potentially important determinants of reserve value prevailing on the deal's announcement date: expected future petroleum prices, and measures of political risk. We constructed two proxies for price expectations: the futures strip prices for oil and gas traded on the New York Mercantile Exchange (NYMEX); and the price of the BP Royalty Trust, a security traded on the New York Stock Exchange (ticker: BPT) since 1989. We calculate the strip prices as averages of futures prices for the nearest 36 months ahead for crude oil and natural gas traded on the NYMEX. For each reserve transaction, a weighted strip price was constructed, with the weights being the percentage of oil and percentage of gas in the reserve. These time series are plotted in Figure 2 along with the spot price of oil. BPT is an unmanaged royalty trust, whose value depends on oil prices over the life of BP's Prudhoe Bay field, the largest in the US.Footnote 12 Expectations of future oil prices determine the value of BPT, and hence can be imputed from BPT market price (Verleger, 1994). For our sample period, however, BPT moved closely with the strip prices, as seen in Figure 2; we report empirical results using only the latter in this paper, although results using BPT are available from the authors upon request.

Petroleum spot prices and measures of price expectations, 2000–2006.

Our measures of political risk are from the ICRG and Institutional Investor. Both use a 100-point scale in which high numbers signify low risk. ICRG distributes (through the PRS Group) a rating of country risk and three sub-ratings – for political, financial, and economic risk – on a monthly basis. We focus on the political risk rating as the subject of interest. This rating is composed of 12 weighted variables covering both political and social attributes, including government stability, socio-economic conditions, investment profile, internal conflict, external conflict, corruption, military in politics, religion in politics, law and order, ethnic tensions, democratic accountability, and bureaucracy quality.Footnote 13 The Institutional Investor rating is based on a semiannual survey of up to 100 bankers from around the world who are asked to rate country creditworthiness. The responses are weighted according to the exposure of the bank and the sophistication of the bank's analytical model to form the Institutional Investor credit rating published in the March and September issues of the magazine.

We match the ICRG and Institutional Investor ratings to each oil reserve transaction based on the most recent March or September rating available on the transaction date. The rating is the one “in effect” on the date of the announcement, and so is released by ICRG or Institutional Investor prior to seeing any public information about the petroleum transaction we study. This timing reduces potential endogeneity empirically; transactors know political risk scores before the transaction is announced, but the producers of the political risk ratings do not observe the transaction before the ratings are announced.Footnote 14 Some transactions span more than one country, in which case we calculate an average of the political risk ratings for the countries involved. (When proportions of reserves in the various countries are known, we calculate a weighted average; when proportions are not known, we calculate an unweighted average.)

RESULTS

Primary Results

The main results from estimating Eq. (4) are contained in Table 2. The dependent variable is either (the log of) the reserve value in the transaction per boe or (the log of) the total value of the transaction per boe. Regressions 1 and 2 consider the model without including political risk ratings. Regressions 3 and 4 utilize the ICRG political risk rating and regressions 5 and 6 utilize the Institutional Investor rating. Table 2 reveals that the results from using the total value of the transaction per boe are quite similar to the results from using the reserve value, suggesting that the distinction between a pure market number and the more meaningful one after an accounting-based adjustment (for any non-reserve components) is not an issue. We therefore focus attention primarily on regressions wherein reserve value is the dependent variable.

Regressions 1 and 2, which omit political risk, explain about 40% of the variation in the dependent variables. Regressions 3–6 add political risk as an explanatory variable, and explain about 50% of the variation in the dependent variables. The increase in the R2 values when political risk variables are added indicates that such variables are important determinants of asset value.

Regressions 7 and 8 add both country- and time-dummy variables (omitting a dummy for 2000 as the reference year); we include dummy variables for all countries involved for transactions with reserves in multiple countries. Country- and time-fixed effects have the advantage of capturing unobserved host-country- and time-specific heterogeneity, and raise regression explanatory power to over 60%. Interpretation of regression coefficients on variables of interest is less clear, however, since these dummy variables may not only serve as controls, but also capture some of the effects of interest. For example, the rising price trend over the period (Figure 2) serves to confound the effects of time and price on reserve value.

In all eight regressions, the elasticity of the value with respect to petroleum price (oil, gas, or both, depending on the asset mix) is positive and statistically significant at the 1% level. In regression 1, a 1% increase in the per-barrel price of oil increases the value of reserves by 1.20%, suggesting that the revenues from extraction increase more than costs. Similar coefficients are found in regressions 2–6. Not surprisingly, given rising prices over time, adding time dummies reduces the price coefficients, as seen in regressions 7 and 8.

Dummy variables pertaining to the type of oil reserve are utilized to control for differences in extraction costs vis-à-vis conventional reserves. The coefficients on these nine dummy variables are presented at the bottom of the table. Not all coefficients are statistically significant, although the variables are kept so that a complete set of dummy variables remains intact. All the dummy variables significant at conventional levels (10%, 5%, and 1%) have the expected signs in regressions 1–6. Notable coefficients are on coalbed methane, LNG, and synthetic crude oil, all of which are costlier to produce than conventional oil reserves, and thus depress the value per boe. The main effect of adding country dummies is that some coefficients on reserve types change: coalbed methane is rendered insignificant at all levels; LNG is significant only at the 10% level; and deepwater reserves become surprisingly valuable. In regressions including a political risk variable, pure royalty interest, which has no extraction costs, raises the value per boe approximately 40%.

The coefficient on the dummy variable for heavy oil, our first control variable, is negative (as expected) and statistically significant. The range of coefficients in regressions 3–8 indicates that heavy oil sells at a 36–42% discount, or might involve a combination of lower prices and higher extraction costs that together sum to 36–42%.

The coefficient on the percentage of gas in the transaction as opposed to oil is small but statistically significantly positive. In an all-gas transaction, value per boe is approximately 0.3–0.4% higher than an otherwise similar all-oil transaction. We retain this variable for its statistical significance, although its economic significance is clearly minimal.

The coefficient on the dummy for information being reported by the buyer is statistically significantly negative, and ranges from −0.146 to −0.107. The interpretation of this is that information coming from the buyer is associated with about a 10–15% lower value of the asset, as if buyers are systematically more optimistic than sellers about reserve size (implying that price per boe is lower in buyer-reported transactions), suggesting that both buyers and sellers consider transactions to be “good deals.”

Our main interest is in the coefficients on the political risk ratings. These coefficients are all positive and statistically significant. In regressions 3, 4, and 7, the political risk coefficient indicates that a one-point increase in the ICRG political risk rating is associated with a 2.4–2.9% rise in value per boe. The variable empirically ranges from 42.5 to 93, for a range of 50.5 points. In regressions 5, 6, and 8, the political risk coefficient indicates that a one-point increase in the Institutional Investor risk rating is associated with a 1.4–2.1% rise in value per boe. This variable empirically ranges from 10.5 to 94.2, for a range of 83.7 points, or two-thirds more than the range of the ICRG index. It is thus not very surprising that the coefficient on the Institutional Investor rating is smaller than the coefficient on the ICRG rating.

Robustness Checks Footnote 15

We re-ran our reserve value regressions adding sets of country and time dummies separately, both as a robustness check on our main results, and to respond to the concern regarding interpretation of coefficients when fixed effects are included in the analysis discussed above. The result is that the coefficient on the ICRG rating falls to 0.016 in the country dummy regression, and rises to 0.031 in the time dummy regression, remaining statistically significant at the 1% level. Likewise, the coefficient on the Institutional Investor is 0.020 in the country dummy regression, falling to 0.015 in the time dummy regression, again both statistically significant at the 1% level. These findings confirm that the political risk measures are indeed capturing variation in political risk rather than just broader cross-country differences.

As a separate robustness check, we employ the index of political constraints developed by Henisz (2000, 2002) in place of the ICRG and Institutional Investor measures of political risk. The political constraints index captures the ease (or difficulty) of a government's changing policy, by focusing on the number and independence of political institutions in a country, as well as the extent to which these institutions are aligned politically. Countries with stronger checks on governmental ability to change policy receive higher scores. Researchers have used the index to proxy for policy stability (Vaaler & Schrage, 2009) and for political commitment to investor protection (Andonova & Diaz-Serrano, 2009).Footnote 16

The political constraints index has four important advantages over the political risk measures we use above. First, it corresponds directly to the concerns of foreign investors that host governments will change the rules of the game once FDI is in place. Second, it is transparent and objective, based on publicly available information on institutional differences among nations, rather than political risk analysts’ subjective judgment. Third, it reflects a structural model of political decision-making (Henisz, 2000, 2002). Finally, it is constructed without reference to the petroleum sector, thereby ensuring exogeneity.

For our analysis, however, a political constraints index has several limitations. First, it addresses an important dimension of political risk – policy risk (Holburn & Zelner, 2009) – but not sources of risk such as civil unrest, conflict between states, or inability of host countries to protect property rights. Especially in natural-resource-rich countries, such risk may stem from rent-seeking by actors other than host-country public officials, notably foreign governmentsFootnote 17 and NGOs seeking local control over operations or resource revenueFootnote 18 (Collier, Hoeffler, & Rohner, 2009). Second, the index does not reflect the orientation along the political spectrum of the host government. Third, because the political constraints index is not released on a regular schedule, it is difficult to know what information is available to managers at the time they negotiate deal terms. Finally, the index is not available in a timely fashion: as of mid-2009, the most recent published data cover 2004.

The latter two concerns imply that asset values are likely to reflect cross-country but not time-series variation in the index. We thus use the average political constraint scores for each country for the period covered by our data for which the index is available, 2000–2004. Using the two measures for each country (one includes judicial and federal constraints, the other does not), we obtain results similar to those reported in Table 2: countries with a higher level of political constraints are associated with greater reserve values.

Political Risk Discounts

The coefficients on the political risk ratings in Table 2 can be used to estimate the discount on oil and gas reserves associated with the riskiness of the country in which the reserves are located. For example, we can consider what the reserves in risky countries would be worth if they were instead located in the United States. Table 3 presents the results.

In the ICRG index, the US has a weighted-average rating of 83 (recall that each country's risk ratings change over time; the weights are the number of transactions occurring within a time period as a proportion of all transactions for the country). Although we use the US as the benchmark, several countries are viewed by ICRG as safer than the US, and have higher political risk ratings. These include Canada, the UK, Norway, Australia, the Netherlands, Denmark, Ireland, and New Zealand. Denmark and New Zealand have the highest weighted-average rating, at 91. Other countries can be considered based on their distance from the US rating of 83. The average rating for Russia, for example, is 63. We may naturally ask what the discount on Russian oil and gas is, based on the gap of 20 points: this discount is (20)(0.029)=58% using the model without fixed effects, and (20)(0.024)=48% under the fixed-effects model. In other words, reserves in Russia trade at a 48% or 58% discount compared with what they would fetch if they were in the United States. Table 3 presents our estimated discounts on oil and gas assets using the two models (corresponding to regressions 3 and 7 in Table 2) for all host countries. On the whole, the numbers are very large, indicating that political risk is an important determinant of value.

In the Institutional Investor index, the US has a weighted-average rating of 93. A few countries have this rating as well (the UK, the Netherlands, and France), but no countries have a higher rating. The average rating for Russia is 42, for a gap of 51 points. The discount for Russian assets compared with what they would fetch if they were in the United States is thus (52)(0.014)=74% without fixed effects, and (52)(0.021)=113% with fixed effects. The greater discount results from Institutional Investor's viewing Russia as riskier relative to the US than does ICRG.

Dependence of Political Risk on Petroleum Price

The regression specification above and Table 2 are consistent with conventional wisdom in the field of political risk analysis: discounts depend on characteristics of the countries rated, not on conditions in the world market. Is political risk moderated by world petroleum prices, as suggested in the initial quote in the paper? We examine interaction effects through a specification that considers the hypothesis that the discount for political risk depends on petroleum prices.

Table 4 presents results from this alternative specification of the model in which there is an interaction between the price of oil and the risk rating. We formulate the interaction by inverting the political risk scale and multiplying by the strip price, or (100 – rating)[ln(strip price)]. If political risk is higher when the price of oil is high, the interaction term will have a negative coefficient. The results in Table 4 convincingly support the intuition that the discount for political risk is higher when the price of oil is high.

Regressions 9, 10, and 13 in Table 4 use the ICRG index of political risk. The mean of the log of the strip price is 3.48 (or $32.46 per barrel), and the mean of the ICRG index is approximately 83 (which is the average for the US alone also). At these means, and using the coefficients in the no-fixed-effects model (regression 9), the elasticity of reserve value with respect to oil price is1.907−0.039 × (100−83)=1.244, about the same as the value of 1.241 reported in regression 3. Likewise, in the fixed-effects model (regression 13), this elasticity is 1.103−0.036 × (100−83)=0.491, close to the value of 0.528 reported in regression 7. The lower elasticity estimates in the fixed-effects models are the result of time dummies capturing the effect of higher prices.

The no-fixed-effects model estimate of the effect of a one-point increase in the ICRG index on reserve value is −0.101+0039 × 3.48 0.035, or 3.5%; the corresponding fixed-effects model estimate is −0.087+0.036 × 3.48=0.038, or 3.8%. These estimates differ somewhat from the values 0.029 and 0.024 reported in regressions 3 and 9, respectively, suggesting that the effects reported in Table 2 may be understated, because interactions between political risk and market prices are ignored.

Fluctuations around the means are of particular note for high-risk countries. For example, in Russia, a country with an ICRG rating of 63, the elasticity of reserve value with respect to oil price is very low, at 0.464 in the no-fixed-effects model. This indicates that a 1% increase in the per-barrel price of oil increases the value of reserves by just under 0.5%. In other words, less than half of the benefits of the price increase accrue to the owner of the reserve. This is consistent with a story in which the government intervenes in the oil industry more when the price of oil is high. (The fixed-effects model produces a nonsensical elasticity less than zero.)

At the average price of oil, the discount on reserves in Russia compared with the US is 69% (no-fixed-effects model) or 77% (fixed-effects model). However, if the price of oil is $25 per barrel, or about half a standard deviation below the mean, the discount on reserves in Russia is just (20)[−0.101+0.039 × ln(25)]=52% under the no-fixed-effect model, or (20)[−0.087+0.036 × ln(25)]=55% under the fixed-effects model. If the price of oil is $40 per barrel, or about half a standard deviation above the mean, the discount on reserves in Russia is an astonishing 88–89% under both models. Table 5 illustrates the discount for all countries under the scenarios of $25 per barrel and $40 per barrel, corresponding to about half a standard deviation above and below the mean strip price.

Regressions 11, 12, and 14 in Table 4 use the Institutional Investor index of risk, which has a mean of 86. Noting that the coefficients on the index are statistically insignificant, we focus attention on the interaction term. Using the coefficients in the no-fixed-effects model (regression 11), the elasticity of reserve value with respect to oil price is 1.233−0.010 × (100−86)=1.093, close to the value α=1 in Eq. (4) above; a 1% increase in market price leads to a 1% rise in reserve value. Likewise, in the fixed-effects model (regression 14) this elasticity is 0.500−0.008 × (100−86)=0.388: a 1% increase in price leads to a 0.4% rise in reserve value. A one-point increase in the Institutional Investor index raises the reserve value by 0.010 × 3.48=3.5% in the no-fixed-effects model or 0.008 × 3.48=2.8% in the fixed-effects model. An examination of fluctuations around these means provides results similar to those found above for the ICRG index. In the Institutional Investor index, Russia has a rating of 42, so the elasticity of reserve value with respect to oil price is 0.653 in the fixed-effects model or 0.036 in the fixed-effects model. At the average price of oil, the discount on reserves in Russia compared with the US is over 100% in both models, reflecting the fact that our simple constant elasticity model breaks down for very large changes.

SUMMARY AND CONCLUSION

This paper has demonstrated that political risk destroys asset value, and that the extent of such value destruction is substantial. Specifically, the paper has calculated the discount on petroleum reserve transactions due to political risk. The first finding is that indices of political risk are significant determinants of the per-barrel value of petroleum reserves. For example, a one-point increase in the ICRG political risk index (signifying a reduction in risk) is associated with a 2.4–2.9% rise in value.

Our findings are relevant to both practitioners and researchers interested in political risk more broadly. The bulk of FDI is through mergers and acquisitions, and managers need to assess political risk discounts in valuing potential target assets. To both practitioners and researchers, market-based discounts offer an alternative to the subjective measures now in use. Our methodology is particularly applicable to industries producing homogeneous commodities, such as agriculture, natural resources, steel, and semiconductors.

Of course, estimates of the discount are only as good as the measurements of risk employed. The ICRG and Institutional Investor indices are subjective, and are not exclusively for the petroleum sector, so some care must be exercised in interpreting the results. Finding a discount suggests that the indices contain valuable information, and that host-country political risk acts like an additional cost of doing business.

A second, more important finding is that political risk and market risk are interrelated. In contrast to what is typically assumed in the literature, we conclude that political risk and market risk cannot be assessed separately, and we demonstrate how to account for their interactions. Our empirical findings confirm the view that political risk depends on market conditions: as assets become more valuable owing to market conditions, a greater fraction of their value is destroyed by political risk. For example, if the price of oil is $25 per barrel, the discount on reserves in Russia is just 52% using the ICRG political risk measure; however, if the price of oil is $40 per barrel, the discount is 88%.

The results in this paper answer some questions while raising others. What other variables would help explain the value of petroleum reserves? The regressions explain slightly more than 60% of the variation in the per-barrel value of the reserves, so more work could be done to find additional determinants. To the extent that any missing variables are correlated with the political risk indicators, they may provide partial explanations of the discount and reduce the significance of the political risk measures. However, our understanding of political risk would be improved. Similarly, the simple constant-elasticity functional form we employ should be considered as an approximation: it breaks down for large changes. A more realistic model may come at the cost of increased complexity, however.

In line with this discussion of omitted variables, it is worth noting that there are alternative explanations for the political risk discount documented. Some relate directly to differences in cost and jurisdictional treatment. Since we are not able to control for transportation costs to get the petroleum to the final consumer, our political risk discount may capture higher transportation costs from countries that happen to be both remote from refining and consuming centers, and politically risky. This is unlikely to be an important effect, however, as transport costs in this industry are low, and petroleum is routinely shipped very long distances. Similarly, since we have not been able to control for tax rates in the host country, our political risk discount may capture higher tax rates in countries that happen to be politically risky. We think this would be too much of a coincidence, but cannot be sure until the issues are empirically investigated. Fiscal treatment of this industry tends to be complex, non-linear, and idiosyncratic, and hence difficult to compare across tax jurisdictions.Footnote 19

A second unanswered question concerns the factors driving the political risk discount. In focusing on the effects of political risk on investment, we have ignored the causes. Is the discount due to poor institutions or excessive government regulation? Is it due to corruption and the cost of bribe payments? Is it due to civil conflict or socio-cultural factors, rather than the threat of government intervention? Some insight may be gleaned by looking at the components of the ICRG political risk index. Other data sources may prove useful as well, particularly given the recent attention to measuring institutional strength and costs of doing business generally (e.g., Kaufmann, Kraay, & Mastruzzi, 2008; La Porta, Lopez-de-Silanes, Shleifer, & Vishny, 2002). Such questions suggest that the area is fertile for future research.

Another issue not considered here is whether the costs of political risk imposed on the resource extraction sector are associated with any benefits elsewhere in the economy. After all, governments may engage in resource nationalism in order to redirect resources to other uses. Some effects may be direct, perhaps if political risk subsequently increases domestic employment or reinvestment of profits locally. Some may be indirect, perhaps if the threat of intervention increases the government's bargaining power such that the company becomes a better corporate citizen offering more social programs. Perhaps the entire discount simply represents the total of bribes required in politically risky countries, such that there is a transfer of wealth from the owner of the petroleum reserve to the bribe-taking officials – but no net change in national welfare. We approach the cost of political risk as if it is a deadweight loss to society, but alternative explanations are possible, and future research may fruitfully engage in a search for benefits.

A final avenue for future research starts by noting that the approach in this paper portrays political risk in the host country as a cost to all firms operating in the country, including both domestic- and foreign-owned firms. In this regard, the topic is an international business topic more by the global nature of the industry and cross-country variation in political risk than by any specific cross-border operations of firms. In other words, this paper is about the overall cost of political risk, rather than the liability of foreignness. A fertile exercise for future research would be to separate the transactions studied into domestic-only and cross-border categories and investigate whether there is any difference.

Other extensions of this idea are possible. For example, further examination of resource nationalism might entail an inquiry into valuation effects when a state-owned enterprise is the buyer or the seller. Do state-owned enterprises pay more or less when they acquire reserves? Do they receive more or less when they sell reserves? Further examining the participants in the transactions may yield useful insights into the market, political risk, and international business.

Notes

A justification for resource nationalism from a practitioner is illustrative: “In less than three years of exploitation, the consortium has earned $5 bn for a $3 bn investment. In contrast, Chad has just received crumbs: $588 m.” Idriss Deby (president of Chad), quoted in Miarom (2006).

“These companies had much greater apprehension concerning the possibility of expropriation and they mentioned more frequently than other groups a favorable foreign tax situation” (Barlow & Wender, 1955: 128). An early teaching case on resource nationalism (Harvard Business School, 1974–1976) examines the Bougainville Copper Mine in Papua New Guinea.

This interaction takes many forms far less dramatic than expropriation. For example, Jones (1984) and Makhija (1993) examine government intervention in the Venezuelan petroleum industry in the period prior to nationalization.

Berry and Wright (2001) summarize the literature on financial statement disclosures of petroleum reserves. These are analogous to asset restatements in manufacturing firms (Francis, Hanna, & Vincent, 1996).

Values are converted from local currency to US$ using exchange rates on the day of the announcement. The former deal's reserves are primarily in Norway, the latter's in the Russian Far East. See the discussion of the two deals in Timmons (2006) and Crooks and Ostrovsky (2006), respectively.

The political risk literature is extensive. Recent examples include Desai, Foley and Hines (2008) and Vaaler (2008) on managerial decisions, and Alfaro, Kalemli-Ozcan, and Volosovych (2008) on cross-border capital flows.

Adelman, De Silva, and Koehn (1991), Thompson (2001), and Adelman and Watkins (2005) test the theory using reserve data from US petroleum-reserve transactions. Adelman and Watkins (1995) use a sample of 34 Canadian reserve transactions. These articles all find that the data are not consistent with the predictions of the simplest version of the Hotelling (1931) theory.

A small literature (e.g., Harris & Ohlson, 1987; Magliolo, 1986; Miller & Upton, 1985; Thompson, 2001) focuses on book value and market value information in US petroleum exploration and production firms’ 10-K filings, rather than market transactions.

Royalty interests belong to the owner of the subsurface rights, typically the owner of the land underneath which the reserve lies, but can be sold to third parties. Non-royalty interests are referred to as “working interests”.

We are indebted to JSH for access to their transactions database.

Smaller deals tend to be less well documented, and we do not include them in our analysis. The JSH database includes deals under $10 million, but JSH does not include them in its reports on transaction activity.

We are grateful to Energy Security Analysis Inc. for providing strip data. BPT data are from DataStream.

For more information, see www.prsgroup.com. The fact that these variables are not based on asset prices or petroleum reserve values implies that endogeneity between petroleum reserve values and the political risk score is unlikely to be a problem.

Because transactions are acquisitions of assets or companies, rather than greenfield investment, they are not public information prior to their announcement dates. The larger issue that political risk in petroleum-based economies may itself arise from the petroleum sector is one that we cannot control for empirically using ICRG and Institutional Investor data; we consider the possibility of such simultaneity in the section on robustness checks below. We thank an anonymous referee for calling our attention to the endogeneity issue.

We are grateful to the editor (Witold Henisz) and referees for their suggestions on this section.

The database and supporting documentation are taken from the website http://www-management.wharton.upenn.edu/henisz/.

Petroleum reserves offshore may be under shared or disputed waters (e.g., Caspian Sea, Gulf of Guinea, South China Sea, Timor Sea).

For example, the Movement for the Emancipation of the Niger Delta in Nigeria.

Johnston (2008) provides insight into recent fiscal evolution and complexity in the industry.

References

Adelman, M. A., & Watkins, G. C. 1995. Reserve asset values and the Hotelling valuation principle: Further evidence. Southern Economic Journal, 61 (3): 664–673.

Adelman, M. A., & Watkins, G. C. 2005. US oil and natural gas reserve prices, 1982–2003. Energy Economics, 27 (4): 553–571.

Adelman, M. A., De Silva, H., & Koehn, M. F. 1991. User cost in oil production. Resources and Energy, 13 (3): 217–240.

Alfaro, L., Kalemli-Ozcan, S., & Volosovych, V. 2008. Why doesn’t capital flow from rich to poor countries? An empirical investigation. Review of Economics and Statistics, 90 (2): 347–368.

Andonova, V., & Diaz-Serrano, L. 2009. Political institutions and telecommunications. Journal of Development Economics, 89 (1): 77–83.

Bailey, W., & Chung, Y. P. 1995. Exchange rate fluctuations, political risk, and stock returns: Some evidence from an emerging market. Journal of Financial and Quantitative Analysis, 30 (4): 541–561.

Bannon, I., & Collier, P. 2003. Natural resources and violent conflict: Options and actions. Washington, DC: World Bank.

Barlow, E. R., & Wender, I. T. 1955. Foreign investment and taxation. Englewood Cliffs, NJ: Prentice-Hall.

Beaulieu, M.-C., Cosset, J.-C., & Essaddam, N. 2005. The impact of political risk on the volatility of stock returns: The case of Canada. Journal of International Business Studies, 36 (6): 701–718.

Beaulieu, M.-C., Cosset, J.-C., & Essaddam, N. 2006. Political uncertainty and stock market returns: Evidence from the 1995 Quebec referendum. Canadian Journal of Economics, 39 (2): 621–642.

Berry, K. T., & Wright, C. J. 2001. The value relevance of oil and gas disclosures: An assessment of the market's perception of firms’ effort and ability to discover reserves. Journal of Business Finance & Accounting: 28 (5–6): 741–769.

Berry, K. T., Hasan, T., & O’Bryan, D. 1998. Relative information content of proven reserves: The BOEs-revenue versus BOEs-energy. Journal of Energy Finance & Development, 3 (1): 1–11.

Bilson, C. M., Brailsford, T. J., & Hooper, V. C. 2002. The explanatory power of political risk in emerging markets. International Review of Financial Analysis, 11 (1): 1–27.

Block, S. A., & Vaaler, P. M. 2004. The price of democracy: Sovereign risk ratings, bond spreads, and political business cycles in developing countries. Journal of International Money and Finance, 23 (6): 917–946.

Boubakri, N., Cosset, J.-C., & Smaoui, H. 2009. Credible privatization and market sentiment: Evidence from emerging bond markets. Journal of International Business Studies, 40 (5): 840–858.

Brunet, A., & Lentini, J. A. 2007. Arbitration of international oil, gas, and energy disputes in Latin America. Northwestern Journal of International Law & Business, 27 (3): 591–630.

Chinn, M. D., LeBlanc, M., & Coibion, O. 2005. The predictive content of energy futures: An update on petroleum, natural gas, heating oil, and gasoline. NBER Working Paper Series, No. 11033.

Click, R. W. 2005. Financial and political risks in US direct foreign investment. Journal of International Business Studies, 36 (5): 559–575.

Collier, P., Hoeffler, A., & Rohner, D. 2009. Beyond greed and grievance: feasibility and civil war. Oxford Economic Papers, 61 (1): 1–27.

Cosset, J.-C., & Rianderie, B. D. 1985. Political risk and foreign exchange rates: An efficient-markets approach. Journal of International Business Studies, 16 (3): 21–55.

Cosset, J.-C., & Roy, J. 1991. The determinants of country risk ratings. Journal of International Business Studies, 22 (1): 135–142.

Crooks, E., & Ostrovsky, A. 2006. Shell learns cold reality of Sakhalin deals. Financial Times, 22 December: 19.

Desai, M. A., Foley, C. F., & Hines, J. R. 2008. Capital structure with risky foreign investment. Journal of Financial Economics, 88 (3): 534–553.

Diamonte, R. L., Liew, J. M., & Stevens, R. L. 1996. Political risk in emerging and developed markets. Financial Analysts Journal, 52 (3): 71–76.

Erb, C. B., Harvey, C. R., & Viskanta, T. E. 1996. Political risk, economic risk, and financial risk. Financial Analysts Journal, 52 (6): 29–46.

Francis, J., Hanna, J. D., & Vincent, L. 1996. Causes and effects of discretionary asset write-offs. Journal of Accounting Research, 34 (Supplement): 117–134.

Ghicas, D., & Pastena, V. 1989. The acquisition value of oil and gas firms: The role of historical costs, reserve recognition accounting, and analysts’ appraisals. Contemporary Accounting Research, 6 (1): 125–142.

Harris, T. S., & Ohlson, J. A. 1987. Accounting disclosures and the market's valuation of oil and gas properties. Accounting Review, 62 (4): 651–670.

Harvard Business School. 1974–1976. Bougainville Copper Ltd Case 9-174-104.

Henisz, W. J. 2000. The institutional environment for economic growth. Economics and Politics, 12 (1): 1–31.

Henisz, W. J. 2002. The institutional environment for infrastructure investment. Industrial and Corporate Change, 11 (2): 355–389.

Holburn, G. L. F., & Zelner, B. A. 2009. Political capabilities, policy risk, and international investment strategy: Evidence from the global electric power industry. Working Paper, Duke University.

Hotelling, H. 1931. The economics of exhaustible resources. Journal of Political Economy, 39 (2): 137–175.

Howell, L. D. 2006. The handbook of country and political risk analysis, (3rd ed.) East Syracuse, NY: The PRS Group.

Johnston, D. 2008. Changing fiscal landscape. Journal of World Energy Law and Business, 1 (1): 31–54.

Jones, R. J. 1984. Empirical models of political risks in US oil production operations in Venezuela. Journal of International Business Studies, 15 (1): 81–95.

Kaufmann, D., Kraay, A., & Mastruzzi, M. 2008. Governance matters VII: Aggregate and individual governance indicators, 1996–2007. World Bank Policy Research Working Paper 4654, June.

Kobrin, S. J. 1979. Political risk: A review and reconsideration. Journal of International Business Studies, 10 (1): 67–80.

Kobrin, S. J. 1980. Foreign enterprise and forced divestment in LDCs. International Organization, 34 (1): 65–88.

Kobrin, S. J. 1984a. Expropriation as an attempt to control foreign firms in LDCs: Trends from 1960 to 1979. International Studies Quarterly, 28 (3): 329–348.

Kobrin, S. J. 1984b. The nationalization of oil production, 1918–1980. In D. W. Pearce, H. Siebert & I. Walter (Eds), Risk and the political economy of resource development: 137–164. New York: St Martin's Press.

Kobrin, S. J. 1985. Diffusion as an explanation of oil nationalization. Journal of Conflict Resolution, 29 (1): 3–32.

La Porta, R., Lopez-de-Silanes, F., Shleifer, A., & Vishny, R. 2002. Investor protection and corporate valuation. Journal of Finance, 57 (3): 1147–1170.

Magliolo, J. 1986. Capital market analysis of reserve recognition accounting. Journal of Accounting Research, 24 (3): 69–108.

Makhija, M. 1993. Government intervention in the Venezuelan petroleum industry: An empirical investigation of political risk. Journal of International Business Studies, 24 (3): 531–555.

Miarom, B. 2006. Chad president orders Chevron, Petronas to leave. Reuters News, 26 August.

Miller, M., & Upton, C. 1985. A test of the Hotelling valuation principle. Journal of Political Economy, 93 (1): 1–25.

Petroleum Intelligence Weekly. 2007a. Resource nationalism: Then and now. 8 January: 5.

Petroleum Intelligence Weekly. 2007b. Sparks fly over soaring project costs. 1 January: 5.

Phillips-Patrick, F. J. 1989. The effect of asset and ownership structure on political risk: Some evidence from Mitterrand's election in France. Journal of Banking and Finance, 13 (4–5): 651–671.

Stevens, P. 2008. National oil companies and international oil companies in the Middle East: Under the shadow of government and the resource nationalism cycle. Journal of World Energy Law and Business, 1 (1): 5–30.

Thompson, A. 2001. The Hotelling principle: Backwardation of futures prices and the values of developed petroleum reserves – The production constraint hypothesis. Resource and Energy Economics, 23 (2): 133–156.

Timmons, H. 2006. Statoil will buy rival's energy units to create world's largest offshore operator. New York Times, 10 December: C3.

United Nations. 2008. World investment report. Geneva: UNCTAD.

Vaaler, P. M. 2008. How do MNCs vote in developing country elections? Academy of Management Journal, 51 (1): 21–43.

Vaaler, P. M., & Schrage, B. N. 2009. Residual state ownership, policy stability and financial performance following strategic decisions by privatizing telecoms. Journal of International Business Studies, 40 (4): 621–641.

Vaaler, P. M., Schrage, B. N., & Block, S. N. 2005. Counting the investor vote: Political business cycle effects on sovereign bond spreads in developing countries. Journal of International Business Studies, 36 (1): 62–88.

Verleger, P. K. 1994. Adjusting to volatile energy prices. Washington, DC: Institute for International Economics.

Vernon, R. 1971. Sovereignty at bay: The multinational spread of US enterprise. New York: Basic Books.

Wälde, T. W. 2008. Renegotiating acquired rights in the oil and gas industries: Industry and political cycles meet the rule of law. Journal of World Energy Law and Business, 1 (1): 55–97.

Weiner, R. J. 2005. Speculation in international crises: report form the Gulf. Journal of International Business Studies, 36 (5): 576–587.

Acknowledgements

We are grateful to Chris Ruppel, John S. Herold Inc., Energy Security Analysis Inc., and Petroleum Intelligence Weekly for data; however, use of the data to examine political risk is solely our responsibility. We are also grateful to the editor (Witold Henisz), referees, and participants at the Fifth JIBS Emerging Frontiers Conference, the Temple International Business Research Forum, Wesleyan University, HEC Montréal, and the AIB, ASSA, and FMA annual meetings for comments. We thank the GW-CIBER for research support.

Author information

Authors and Affiliations

Corresponding author

Additional information

Accepted by Witold Henisz, Area Editor, 28 July 2009. This paper has been with the authors for three revisions.

Rights and permissions

About this article

Cite this article

Click, R., Weiner, R. Resource nationalism meets the market: Political risk and the value of petroleum reserves. J Int Bus Stud 41, 783–803 (2010). https://doi.org/10.1057/jibs.2009.90

Received:

Revised:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1057/jibs.2009.90