Abstract

In for-profit organizations efficiency measurement with reference to the potential for profit augmentation is particularly important as is its decomposition into technical, and allocative components. Different profit efficiency approaches can be found in the literature to measure and decompose overall profit efficiency. In this paper, we highlight some problems within existing approaches and propose a new measure of profit efficiency based on a geometric mean of input/output adjustments needed for maximizing profits. Overall profit efficiency is calculated through this efficiency measure and is decomposed into its technical and allocative components. Technical efficiency is calculated based on a non-oriented geometric distance function (GDF) that is able to incorporate all the sources of inefficiency, while allocative efficiency is retrieved residually. We also define a measure of profitability efficiency which complements profit efficiency in that it makes it possible to retrieve the scale efficiency of a unit as a component of its profitability efficiency. In addition, the measure of profitability efficiency allows for a dual profitability interpretation of the GDF measure of technical efficiency. The concepts introduced in the paper are illustrated using a numerical example.

Similar content being viewed by others

References

Ali AI and Seiford LM (1993). The mathematical programming approach to efficiency analysis. In: Fried HO, Lovell CAK and Schmidt SS (eds). The Measurement of Productive Efficiency: Techniques and Applications. Oxford University Press, New York, Oxford, pp. 120–159.

Balk BM (2001). Scale efficiency and productivity change. J Prod Anal 15: 159–183.

Banker RD (1984). Estimating most productive scale size using data envelopment analysis. Euro J Opl Res 17: 35–44.

Banker RD and Maindiratta A (1988). Nonparametric analysis of technical and allocative efficiencies in poduction. Econometrica 56: 1315–1332.

Berger AN, Hancock D and Humphrey DB (1993). Bank efficiency derived from the profit function. J Bank Fin 17: 314–347.

Berger AN and Mester LJ (2000). Inside the black box; what explains differences in the efficiencies of financial institutions? In: Harker PT and Zenios SA (eds). Performance of Financial Institutions: Efficiency, Innovation and Regulation. Cambridge University Press, Cambridge, UK, pp 93–150.

Chambers RG, Chung Y and Färe R (1996). Benefit and distance functions. J Econ Theory 70: 407–419.

Chambers RG, Chung Y and Färe R (1998). Profit, directional distance functions, and Nerlovian efficiency. J Optim Theory and Appl 98: 351–364.

Charnes A, Cooper WW and Rhodes E (1978). Measuring efficiency of decision making units. Eur J Opl Res 2: 429–444.

Charnes A, Cooper WW, Golany B and Seiford L (1985). Foundations of data envelopment analysis for Pareto-Koopmans efficient empirical production functions. J Econom 30: 91–107.

Coelli T, Grifell-Tatje and Perelman S (2002). Capacity utilisation and profitability: a decomposition of short run profit efficiency. Int J Product Econ 79: 261–278.

Cooper WW, Park KS and Pastor JT (1999). RAM: a range adjusted measure of inefficiency for use with additive models, and relations to other models and measures in DEA. J Product Anal 11: 5–42.

Cooper WW, Seiford LM and Tone K (2000). Data Envelopment Analysis: A Comprehensive Text with Models, Applications, References and DEA-Solver Software. Kluwer Academic Publishers: Boston.

Färe R, Grosskopf S and Lee H (1990). A nonparametric approach to expenditure constrained profit maximization. Am J Agri Econ 12: 574–581.

Färe R, Grosskopf S and Lovell AK (1994). Production Frontiers. Cambridge University Press: UK.

Färe R, Grosskopf S and Lovell CAK (1985). The Measurement of Efficiency of Production. Kluwer-Nijhoff Publishing: Boston.

Färe R, Grosskopf S and Zelenyuk V (2002). Finding common ground: efficiency indices Paper presented at the North American Productivity Workshop at Union College, Schenectady, NY.

Färe R and Lovell CAK (1978). Measuring the technical efficiency of production. J Econo Theory 19: 150–162.

Kumbhakar SC (2001). Estimation of profit functions when profit is not maximum. Am J Agri Econ 83: 1–19.

Kuosmanen T (1999). Some remarks on scale efficiency and returns to scale in DEA. Helsinki School of Economics and Business Administration, Helsinki.

Lovell CAK and Sickles RC (1983). Testing efficiency hypothesis in joint production: a parametric approach. Rev Econ Stat 65: 51–58.

Pastor JT, Ruiz JL and Sirvent I (1999). An enhanced DEA Russell graph efficiency measure. Eur J Opl Res 115: 596–607.

Portela MCAS and Thanassoulis E (2005). Profitability of a sample of Portuguese bank branches and its decomposition into technical and allocative components. Eur J Opl Res 162: 850–866.

Russell RR (1985). Measures of technical efficiency. J Econ Theory 35: 109–126.

Tone K (2001). A slacks-based measure of efficiency in data envelopment analsysis. Eur J Opl Res 130: 498–509.

Varian HR (1992). Microeconomic Analysis, 3rd edn. W.W. Norton and Company: New York.

Acknowledgements

We acknowledge the financial support of the Portuguese Foundation for Science and Technology, and the European Social Fund. The contents of the paper are the responsibility of the authors.

Author information

Authors and Affiliations

Corresponding author

Appendix

Appendix

Properties of the geometric distance function defined in model (3)

- G1.:

-

0⩽G(x, y)⩽1

- G2.:

-

G(αx, α−1y)⩽(1/α2) G(x, y), α⩾1 and G(αx, α−1y)⩾(1/α2)G(x, y), α⩽1

- G3.:

-

G(αx, y)⩽(1/α) G(x, y)⩽G(x, y), α⩾1

- G4.:

-

G(x, αy)⩽αG(x, y)⩽G(x, y), 0⩽α⩽1

G1 Proof

-

The GDF cannot be greater than 1. In order for this to happen the numerator in (3) should be greater than the denominator. However, as every θ i in the numerator is ⩽1, and every β r in the denominator is ⩾1, GDF>1 results in an impossibility. This means that the maximum value of G(x, y) is 1, happening when the numerator equals the denominator. As every θ i in the numerator is ⩽1, and every β r in the denominator is ⩾1, the equality between the numerator and denominator can only happen when all θ i and all β r are 1.

The GDF may be zero when some inputs (but not all, as we assume that it is not possible to produce outputs with zero inputs) are zero. For zero outputs the model cannot find a feasible solution as it would be possible to find an infinitely large β ro associated with the zero output.

G2 Proof

-

This property states that G(x, y), satisfies sub-homogeneity (eg Russell, 1985) of −2 degree. Indeed,

G3 and G4 Proof

-

These properties relate with the weak monotonicity properties of the geometric distance function. The input monotonicity implies that

The output monotonicity implies that

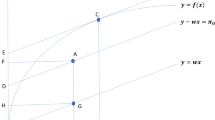

A unit of maximum profitability is always scale efficient

Consider for the single input output case a unit A (x A , y A ) for which y A /x A is maximum (being therefore a CRS efficient unit). If this unit is assessed at prices (p A , w A ) then clearly for this unit's prices p A y A /w A x A >p A y j /w A x j , for every j≠A. Assessing unit B (x B , y B ), for which y B /x B is not maximum, at prices (p B , w B ) we cannot find for this unit's prices p B y B /w B x B >p B y A /w B x A , since y A /x A is maximum. Therefore, the above model (7) renders maximum profitability units that are also scale efficient. This reasoning can be extended to the multiple input/output case since the way we aggregate output revenues and input costs is through the geometric mean. Therefore replacing above p j y j /w j x j by (Π r p rj y rj )1/s/(Π i w ij x ij )1/m maintains the reasoning valid.

Rights and permissions

About this article

Cite this article

Portela, M., Thanassoulis, E. Developing a decomposable measure of profit efficiency using DEA. J Oper Res Soc 58, 481–490 (2007). https://doi.org/10.1057/palgrave.jors.2602166

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1057/palgrave.jors.2602166