Abstract

Social Security and Medicare programs are contributing to the rapidly increasing public debt and continuous budget deficits. The extent of the fiscal imbalance attributed to these programs may substantially exceed the forecasts of the Social Security Administration (SSA) and the most aggressive projections of other organizations. The many advances in biomedical sciences may significantly extend the longevity of the aging population that will by far outpace the planned increases in the retirement age. In this article, we evaluate three hypothetical scenarios where all other factors affecting the demographic distribution remain unchanged, but the mortality rates are decreased taking into consideration the progress in science and technology. Our estimates reveal that if deaths caused by cardiovascular diseases and cancer are eliminated, the fiscal imbalance may be as high as USD 87 trillion in present value. Given the current pace of biological innovations, the likelihood of elimination of those diseases is not improbable, and if that happens the welfare programs may no longer be sustainable. We propose that the forecasting methods of fiscal imbalance should incorporate the progress in medical sciences. The US and other governments may consider proactively increasing the retirement age and accelerating research in biomedical sciences with the goal to extend healthy working life span to keep pace with the decreases in mortality.

Similar content being viewed by others

INTRODUCTION

The structural imbalance of Social Security and Medicare programs

Social Security provides enrollers, their spouses and, in some instances, their child dependants retirement and disability insurance, as well as other benefits. Primarily, however, Social Security provides a fundamental source of income to retirees and it has played a significant role in the reduction of elderly poverty within the country.1 Social Security is primarily financed through payroll taxes contributed by both employers and employees. After a number of years, participants who are fully insured are legally entitled to the proceeds of the funds to which they and their employers have funded. Practically, individuals are eligible to receive Social Security funds after 40 calendar quarters.2

Although the program is a hugely important safety net for Americans, the financial future of US Social Security and Medicare programs is subject to serious issues that could ultimately lead to the insolvency of the Social Security Fund. The Social Security Administration (SSA)'s trustee report (2012)3 noted that actuarial deficits of Social Security and Medicare programs substantially increased in 2012 and attributed this deficit increase to the possible increase in Medicare costs, coupled with changes in Social Security, resulting from decreased payroll tax revenue. The SSA raised serious concerns that Social Security and Medicare programs, which accounted for approximately 36 per cent of the 2011 federal expenditure, are likely unsustainable under prevailing financial conditions and legislative policies. Similar concerns have been extensively discussed by Brown et al,4 Kotlikoff,5 and Gokhale and Smetters,2, 6 among many others.

The receipts-expenditure imbalances of the Social Security program primarily occur because of the dramatic demographic changes engendered by the retiring Baby Boomer population. Over the next 50 years, a significant portion of this population will be entitled to collect benefits, which will increase the dependency ratio. Although this generation significantly contributed to the labor force, their retirement will drastically decrease the revenue available to provide payouts. Subsequently, the taxpaying base will drastically dwindle upon Baby Boomer retirement.

The equation goes far beyond the Baby Boomer phenomenon. Indeed, biomedical advances have significantly reduced mortality rates, and over the last 50 years life expectancy has increased by more than 10 years. However, retirement age has not changed much: the consequence is a strong imbalance from longer retirements.

In addition, and possibly in line with the reduced mortality rates, global fertility decreased from five to two and a half children per female.7 This has strong implications for Social Security as the present social structure is based on a generational framework in which individuals’ payroll taxes are used to pay for retirees’ benefits.

Last but not least, and again probably in line with longer lives, the length of education has increased, as well as the average age to enter workforce (Fullerton)8. Therefore, improved longevity – the direct result of innovative medical sciences – and other elements that to a large extent are probably a consequence of improved longevity have generated this difficult situation: too few citizens providing receipts during too little time and too many citizens generating expenditures during increasing durations.

Assessing the current state of Social Security

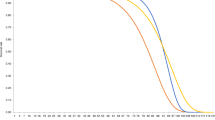

When Social Security was enacted in 1935, this development was not anticipated. At present, the current SSA trustee report (2012),3 coupled with some earlier findings by Gokhale and Smetters,2, 6 provides evidence on the state of imbalance of Social Security and Medicare programs. Figure 1 shows the increasing trend in historical and projected Social Security and Medicare expenses as percentage of GDP.

Social Security and Medicare cost (as a percentage of GDP) (1970–2086). Source: SSA Trustee Report (2012).

One solution is to increase receipts. The SSA expects this percentage of GDP to normalize at least by mid-century; given the current state of economic and political affairs, the additional burden of this imbalance will be borne by the working generation.

However, in this article, we propose that greater consideration and changes are needed to address the situation before deficits start to triple. Indeed, most of the actuarial assumptions related to costs and revenues for Social Security and Medicare programs are based on population growth using historical trends. These projections might be seriously flawed as developments in the medical and health sciences, especially in the mid- to late twentieth century, have started to increase longevity past retirement age, faster than in the past. This trend is likely to continue in the future with further advancement in the biological sciences, which will likely create a significant variance between population projections and actual beneficiaries in the future. The 2011 SSA projections expected the Trust Fund to be depleted by 2036; however, after accounting for actual beneficiaries in 2012, that same trust fund is now expected to be depleted in 2033: simple extrapolations of the past do not seem to be sufficient.

Recent biomedical advances and declining mortality rates

Much of the world's breakthroughs in science and technology that led to the advent of the digital age and globalization occurred in the second half of the twentieth century. The most notable technological advances such as portable electronics and the Internet were widely adopted in the past two decades. Biomedical sciences largely benefit from such advances: research articles accessible to a few on paper are being replaced by online articles accessible to everyone. Research and clinical practice is now communicated and coordinated via online papers, emails, forums, at an unprecedented speed. As a result, there has been considerable progress in biomedical sciences with advances in advanced biomaterials, diagnostics methods, cell, tissue and organ engineering and regeneration, genomics, proteomics and bioinformatics.

We are only starting to see concrete applications because the road to market is much more difficult for biomedical technologies than it is for computer science because they require rigorous validation via the heavily regulated medical industry. Consequently, many of the recent technologies that possess the potential to significantly extend healthy life spans remain at the laboratory level. However, with the help of aging populations in particular, the amount of funding in the biomedical sciences has been increasing at an unprecedented rate.

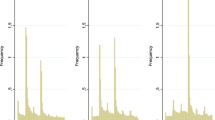

Figure 2 illustrates well the rate at which knowledge and funding in biomedical sciences is progressing. It is reasonable to expect that these investments will yield longevity dividends in the form of decreases in mortality and increases in healthy life spans in the near future.

Increases in government funding and research articles 1993–2011.Source: These calculations were made using the International Aging Research Portfolio.9 They include NIH, NSF, European Commission, CIHR IRSC Canada and AHR Australia grant data on biomedical sciences.

Some life-extending technologies are already in or nearing mainstream clinical use. Statins, beta-blockers, vasodilators and other pharmaceuticals that significantly extend the survival of patients with cardiovascular conditions became blockbuster drugs with tens of billions of dollars in revenue. The mainstream clinical use of many of these drugs and procedures started less than three decades ago and focused on treating the patient. The focus on patients is a natural starting point, to make health technologies marketable. However, the greater effect is likely to come, when those technologies will be used to prevent the development of the medical condition, before symptoms become troublesome (Table 1).

At present, owing to the relatively short time that such novel drugs and treatments have been available, and because they are still primarily targeted to people with serious health conditions, the effects on life expectancy and demography in general are not yet quantifiable. Consequently, it may take another decade for the longevity revolution to set new standards in life expectancy planning. However, the analogy with strong investments for faster computer chips might become better every year. Indeed, many more potent life-extending technologies are being developed in the R&D arena that require investments to go through validating procedures and reach general population health. The strong pressure of aging populations is likely to provide the required investments and to lead to shorter paths towards marketability.

In this article, we argue that because of increases in the biomedical sciences, and consequently, human longevity, we should expect a significantly higher proportion of aging citizens, which will likely produce additional severe burdens to dwindling funding for Social Security and Medicare programs. The next section will highlight the methodology we will employ to ascertain population projections and provide estimation for the requisite revenue levels to pay out benefits. The subsequent section will provide a discussion of our findings. Summarily, the last section will provide concluding remarks.

METHODOLOGY

Population projections

For the sake of clarity, we will define three simple mortality scenarios in the future, and will keep other assumptions such as fertility and immigration unchanged across the three scenarios. As mentioned in the introduction, increased longevity would actually reinforce the imbalance indirectly, but some associated decisions would be undertaken as a consequence: instead of modeling such details, we will take three clear different scenarios. Depending on what associated actions may be undertaken in the future, the results of the scenarios could be revised up or down.

Our first scenario is a simple extrapolation of the past, where the speed of hygiene and curative medical improvements remain the same as the past despite the unprecedented rate of discoveries of the last decades that are for many still in the lab. We model it with a Lee-Carter model,10 where the exponential decrease of mortality rates for any given age continues at the same pace: ‘mortality improvements of the past remain the same in the future’. We fit the improvement rates for males and for females aged 20 to 100 from 1951 to 2007, based on general US population data extracted from the Human Mortality Database,11 and apply them up to 2080.

In the second scenario, we assume that in the period from 2013 to 2030, there would be a decrease in the overall mortality rate by 50 per cent, following a considerable reduction in the risk of most common cardiovascular diseases and some other common ailments.

To be clear, the quantification of impacts on mortality by some specific biomedical progress is still more art than science. Owing to co-morbidity and disease interactions, some models predict that the elimination of mortality from heart disease could increase life expectancy by 7.5 years.12 Therefore, the calibration of scenario 2 comes from a more global appreciation: a division of mortality rates by two corresponds to an increase of life expectancy by 8 years, or to biomedical improvements of slightly less than four decades so far. The next paragraph gives examples of ongoing biomedical breakthroughs, and we will let the reader judge whether this is sufficiently exceptional in terms of probable impacts to represent in itself several decades of past progress.

Thus, here are examples that may correspond to scenario 2. In a strong technological form, scenario 2 may result from current developments in the growing of vessels and tissue engineering, and the reprogramming of cells after infarction scar formation in full cardiac muscle cells. This would have been science fiction 10 years ago but we now see the first applications in the clinics. Apparently less exceptional but far from insignificant, scenario 2 may also correspond to the application of current life-extending drugs to secondary prevention, instead of limiting the use to patients. That is an ongoing path with the generalization of the use of vasodilators and beta-blockers following light cardiovascular symptoms; or the use of metformin in low educated populations at risk of diabetes. In its much wider form, the concept becomes one of a cheap polypill for anyone aged 55 and above: small doses of medications to reduce blood pressure, blood glucose and LDL cholesterol. Such a strategy was predicted to reduce cardiovascular disease by more than 80 per cent13 and some of the first implementations so far confirm the predictions.14, 15, 16

In scenario 3, we assume that during 2013-2030, the mortality rate will be reduced by 80 per cent. This corresponds to an increase of life expectancy of 18 years and could typically occur with drugs that slow aging17, although targeting diseases does not necessarily lead to slowing aging.

Here are some concrete examples in the form of a 10-year retrospective synthesis. We start with the worm C elegans because, owing to fast life span screenings, it has generated numerous guiding results that apply to mice and humans. Life extension is found to be so plastic that even randomly silencing genes can significantly extend life span; in 2005, 89 such genes are counted.18 Some genes are studied and greater life extensions are observed – up to 10-fold.19 In mice that are also mammals, lifespan can be doubled by a mix of gene change and diet restriction.20 And some long-lived human families are found to naturally have some gene mutations (in genes called ‘FOXO3A’, ‘IGF-1’, ‘AKT’) that were previously shown to extend the life span of mice.21 A large focus is now on drugs, with a starting point in already approved drugs. In 2009, the drug rapamycin was found to increase the life span of mice even when started late in life (Harrison)22. That drug was approved for cancer and other conditions and is widely used in clinical practice. It might be that taking the drug would prolong human life span by 10-30 years, but it has many side effects ‘meanwhile’ and in the end it might also be that it does not prolong life span. Other drugs with very little side effects are very promising and are being tested in various ways. Metformin, the widely used, cheap, anti-diabetic drug, showed promising results in cancer and cardiovascular prevention. Here, we find that scenarios 2 and 3 overlap when considering the assessment of the long-term-health impact of existing drugs (KEHLY, 2012).23 Scenario 3 may also correspond to more disruptive impacts from regenerative medicine and tissue engineering in particular.

For the purpose of our estimation, all three scenarios come with complementary assumptions: the birth rate was assumed to be proportional to the total number of women aged between 20 and 45 years where the coefficient of proportionality is taken to the ratio in 2007. Furthermore, we assumed that migration stabilized at the level of a million people a year, causing sex and age structure not to likely differ from that of the general population. The algorithm for the population estimation is reported in the Appendix.

Estimation of benefits and revenues

We model SSA-based fiscal imbalance as simply the difference between government revenue and expenses related to both Social Security and Medicare programs. The differentiating point between our estimates and those of the SSA (and previously reported in the literature) will be the impact of the aging population with a higher life expectancy and increased health-care costs. Mathematically, the imbalance between receipts and benefits will be represented as:

The present value (PV) of benefits is expected to be greater than the present value of revenues, causing a deficit in already costly and increasingly underfunded Social Security and Medicare programs. Therefore, it is only logical that sweeping policy changes must be made in order to engender the sustainability of these important programs.

In order to estimate this imbalance, we adapt the two population cohorts used and reported by the SSA in their trustee report; these are 20–65 years for the working population, and 65 and older for the beneficiaries. Our projections for these cohorts are a function of an increase in longevity adjusted on a yearly basis. Consequently, we adjust benefits and receipts for Social Security and Medicare programs. The benefits are based on outlays for Social Security and Medicare. The Social Security expenses are calculated for the segment receiving the benefits after the age of 65. The expenses are adjusted for those members of the population who will retire before regular FRA. Medicare expenses will accommodate for both Part A and Part B Medicare facilities. Similarly, the receipts for Social Security are calculated by simply taking the contribution of the working population from payroll taxes and any income taxes paid by the Social Security beneficiaries, Medicare receipts, taxes on benefits, premiums, general revenue and state transfer and drug fees. All estimates for receipts and benefits are extracted from the SSA's website, and we simply adjust for our population projections.

FINDINGS AND DISCUSSION

Size of the imbalance

The decade-long comparative population projections based on our three scenarios and the SSA Trustees Report (2012)3 are reported in Table 2.

Under scenario 1, the total population is approximately 429 million24 by 2080, of which 106 million (∼25 per cent) are aged 65 or older, and 224 million will be of working age. The SSA estimates for intermediate assumptions project that the working population will increase to 251 million, while beneficiaries will be approximately 104 million. In scenario 1, throughout the projection period, our estimates for beneficiaries are similar to those of SSA estimates; however, we observe a variance within working population. This variance will result in a reduction in estimated receipts vis-à-vis the SSA, for Social Security and Medicare, mainly via payroll taxes, which will result in a relatively larger imbalance for these two programs.

In scenario 2, the general population shows a rather moderate increase (∼456 million by 2080, against the ∼429 million in the baseline scenario). There is almost no change in the number of affected children and teenagers (up to 19 years), and we observe only a slight affect in the major category of workers (20–64 years). This is because mortality rates in the categories are already quite low. Conversely, we project that the number of people of retirement age (65 years and older) will increase significantly to 131 million compared with 106 million in scenario 1, and 104 million for SSA estimates. We project that beneficiaries will account for approximately 29 per cent of the total population by the terminal year. In this scenario, where we expect a 50 per cent decline in mortality owing to the elimination of cardiovascular diseases, we expect a significant increase in unfunded Social Security and Medicare benefits liabilities compared with what is currently anticipated and reported in the recent SSA Trustee Report.

Our third scenario is the worst-case scenario for United States. In this scenario, where we expect mortality to decline by 80 per cent owing to the development of geroprotectors, we expect the total population to grow moderately to 480 million by 2080. As mortality rates within the working population are already low, there is no significant change in our estimates for the working-age group. However, the number of people of retirement age will rise significantly to approximately 155 million, accounting for 32 per cent of the total population. If this scenario prevails, we expect that the provision of these vital public goods programs either will cease or be dramatically undercut.

Timing of the imbalance and aggravating factors

On the basis of SSA and our three scenario population estimates, we project the fiscal imbalance of Medicare and Social Security programs as outlined in section ‘Estimation of benefits and revenues’. These comparative figures are presented in Table 3. The SSA reports a surplus of USD 2.8 trillion in 2013 that decreases to a deficit imbalance of USD 5 trillion (917 billion in present value) by 2080. On the basis of the official estimates, the Social Security program has a surplus of receipts over projected benefits with net present value25 of USD 9.5 trillion. An important factor in this estimation is the expectation that the trust fund will continue to support the benefits before it is exhausted in 2033. It is important to note that last year, the SSA expected the fund to be exhausted by 2036.

The situation is particularly suboptimal when we incorporate population mortality factors to estimate the resulting Social Security imbalance. In the first scenario, we expect an imbalance of USD 4.3 trillion in present value that increases to USD 36.9 trillion if mortality decreases by 50 per cent. Further, if we expect the innovation in medical sciences to reduce mortality by 80 per cent, the deficit in present value will rise to USD 66.4 trillion. We expect the trust fund to be exhausted by 2030, 2029 and 2028 for scenario 1, 2 and 3, respectively. For Medicare (Part A and B), official estimates reveal a net present value imbalance of USD 13.3 trillion, whereas in our base case we expect this deficit to trail around USD 13.8 trillion. In scenario 2, we project the deficit to be USD 17.6 trillion, while in the extreme case of 80 per cent decline in mortality we report an expected net imbalance of USD 22.2 trillion. The Medicare-based comparative imbalances are presented in Table 4.

The total liability for Social Security and Medicare programs is presented in Table 5. The official estimates for these unfunded liabilities remain around USD 3.4 trillion. However, we predict that these liabilities will remain between USD 18.1 trillion and USD 87.5 trillion based on various mortality scenarios. The results for Social Security and Medicare imbalance are not surprising in our scenarios. We observe a larger impact in Social Security as compared with Medicare because Social Security benefits are continuous cash flows that will increase with increases in population that is in retirement age. Conversely, Medicare benefits are paid when they are incurred, and in our extreme scenarios, where we expect a drastic decline in mortality rate due to innovation in clinical knowledge, we should also expect a regressive increase in benefit payments related to Medicare, stemming from the elimination of some common but expensive to treat diseases.

Our results are more alarming than earlier evidence by Gokhale and Smetters,2, 6 and Kotlikoff5 who reported likely variance in the financial position of the trust fund and the sustainability of these programs for the public welfare. Gokhale and Smetters2 forecasted a fiscal imbalance of USD 65.9 trillion based upon fiscal and generational imbalance. Our prediction on fiscal imbalance only stands at USD 87.1 trillion for the worst-case scenario.26 None of these earlier studies incorporated the likely scenarios when longevity could increase at a higher pace than is anticipated by SSA population experts owing to dynamic development in the medical sciences.

CONCLUSION

In this article, we interconnect the impact of technological enhancements in the medical sciences on the unfunded liabilities of US Social Security and Medicare programs. We base our findings on three different scenarios that assume varying mortality rates that are linked with the elimination of particularly lethal diseases such as cardiovascular diseases and cancer. If health conditions improve, and these diseases are eliminated Baby Boomers will have a higher longevity and we should expect a fiscal imbalance that can be as high as USD 87.1 trillion in present value. If this occurs, it will raise two questions. First, how can the United States support unfunded liabilities of this scale? Second, will the United States become insolvent if there is a default on these liabilities? Given the present legislation, concerning Social Security and health care, US solvency, and the sustainability of these public programs is critically important but also virtually impossible with the status quo.

Currently, there have been no serious efforts to prepare against the mounting deficit. It is imperative that this issue is addressed via drastic changes to the funding and administration of Social Security via the tax code. It seems inevitable that the retirement age must be immediately increased to significantly over 65 years or even 70. In addition, inroads should be made so that Baby Boomers can be reemployed if ideal fiscal conditions are not met and reality dictates that they must return to work.

Some corrective actions are described. Increasing the age of retirement is not a desirable solution from the personal point of view of most workers. But if governments can accelerate the ongoing longevity revolution, shift the priorities to increasing healthy working life span instead of keeping the patient alive for as long as possible in the later years, and simultaneously increase the age of retirement, the benefits will become obvious. Governments, policy organizations and health-care providers should work together to proactively increase the pension age, promote and foster lifelong learning and career planning, accelerate aging research and make preventative and regenerative medicine readily available. Financial institutions and pension funds should incorporate the effects of the recent biomedical breakthroughs into the forecasting models and, in the short term, consider developing financial vehicles to hedge against increases in longevity to maintain solvency until decreases in mortality turn from a source of economic burden to a source of economic growth.

The strong potential deficit of the Social Security and the Medicare should not be ignored and urgent actions should be taken to prevent the coming crisis.

References and Notes

Engelhardt, V. and Gruber, J. (2004) Social Security and the Evolution of Elderly Poverty. National Bureau of Economic Research Working Paper No. 10466, pp. 1–44.

Gokhale, J. and Smetters, K. (2005) Measuring Social Security's Financial Problems. National Bureau of Economic Research Working Paper, No. 11060, pp. 1–29.

Social Security Administration. (2012) The OASDI Trustees Report. Board of Trustees of the Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds, pp. 1–252.

Brown, J., Clark, R. and Rauh, J. (2011) The economics of state and local pensions. Journal of Pension Economics and Finance 10 (2): 161–172.

Kotlikoff, L. (2006) Is the United States bankrupt? Federal Reserve Bank of St Louis Review 88 (4): 235–249.

Gokhale, J. and Smetters, K. (2003) Fiscal and Generational Imbalances: New Budget Measures for New Budget Priorities. Federal Reserve Bank of Cleveland Policy Discussion Paper 5, pp. 1–44.

Bloom, D., Canning, D. and Fink, G. (2011) Implications of Population Aging for Economic Growth. National Bureau of Economic Research Working Paper No. 16705, pp. 1-36.

Fullerton, H. (1997) Labor force 2006: Slowing down and changing composition. Monthly Labor Review 11: 23–38.

Zhavoronkov, A. and Cantor, C.R. (2011) Methods for structuring scientific knowledge from many areas related to aging research. PLoS ONE 6 (7): e22597.

Lee, R.D. and Carter, L. (1992) Modeling and forecasting U.S. mortality. Journal of the American Statistical Association 87: 659–671.

Human Mortality Database (HMD). website at www.mortality.org where national mortality data are republished for a large number of countries.

Somerville, K. and Francombe, P. (2005) Modeling disease elimination. Journal of Insurance Medicine 37 (1): 13–19.

Wald, N.J. and Law, M.R. (June 2003) A strategy to reduce cardiovascular disease by more than 80%. BMJ 326 (7404): 1419.

Sanz, G. and Fuster, V. (2009) Fixed-dose combination therapy and secondary cardiovascular prevention: Rationale, selection of drugs and target population. Nature Clinical Practice Cardiovascular Medicine 6 (2): 101–110.

Zeymer, U. et al (2011) Effects of a secondary prevention combination therapy with an aspirin, an ACE inhibitor and a statin on 1-year mortality of patients with acute myocardial infarction treated with a beta-blocker. Support for a polypill approach. Current Medical Research & Opinion 27 (8): 1563–1570.

Wald, D.S., Morris, J.K. and Wald, N.J. (2012) Randomized polypill crossover trial in people aged 50 and over. PLoS One 7 (7): e41297.

Martin, G.M., LaMarco, K., Strauss, E. and Kelner, K.L. (2003) Research on aging: The end of the beginning. Science 299 (5611): 1339–1341.

Hamilton, B. et al (2005) A systematic RNAi screen for longevity genes in C. Elegans. Genes & Development 19 (13): 1544–1555.

Ayyadevara, S., Alla, R., Thaden, J.J. and Shmookler Reis, R.J. (2008) Remarkable longevity and stress resistance of nematode PI3K-null mutants. Ageing Cell 7 (1): 13–22.

Bartke, A. and Brown-Borg, H. (2004) Life extension in the dwarf mouse. Current Topics in Developmental Biology 63: 189–225.

Kenyon, C.J. (2010) The genetics of ageing. Nature 464 (7288): 504–512, Review.

Harrison, D. et al (2009) Rapamycin fed late in life extends lifespan in genetically heterogeneous mice. Nature 460 (7253): 392–395.

Debonneuil, E. (2012) KEHLY: European initiative to know effects on healthy life years, https://webgate.ec.europa.eu/eipaha/initiative/index/show/id/5.

For space constraints, we are not reporting year-wise total population estimates and focus on population in two age cohorts. All estimates that are not reported are available on request.

For present value calculation we used effective yield on US Treasury Bonds of various maturities. The results remained similar representing no impact of maturity premium. We are only reporting results for 10-year bond yield discounted back to 2012.

It must be noted that effective yield used by Gokhale and Smetters2 was slightly less than the discount rate we have used, so our estimates are more conservative.

Acknowledgements

The authors would like to thank Dr Ayesha Afzal for assistance in preparing the financial model and Hugh Gallagher of Insurope and IEBA and Geoffrey Furlonger of SPARK Pensions and HR consulting for their valuable advice.

Author information

Authors and Affiliations

Corresponding author

Additional information

1PhD, is a Director and Trustee of the Biogerontology Research Foundation, a UK-based registered charity supporting aging research worldwide, a Director of the International Aging Research Portfolio (IARP) knowledge management project and the Head of NeuroG, a neuroinformatics project intended to assist the elderly suffering from dementia. He also heads the Bioinformatics and Medical Information Technology Laboratory at the Federal Clinical Research Center for Pediatric Hematology, Oncology and Immunology. His primary research interests include systems biology of aging, regenerative medicine, machine learning and economics of aging and longevity. He holds two Bachelor Degrees from Queen's University, a Masters in Biotechnology from Johns Hopkins University and a PhD in Biophysics from the Moscow State University.

2holds a PhD from University of Paris Dauphine in Quantitative Finance. He is associated with The Biogerontology Research Foundation, London, UK and Lahore School of Economics, Pakistan.

Appendix

Appendix

Algorithm

-

1

The starting values for the population Ng x,t are the values in 2007. The fraction βg of male to female newborns is calculated using the number of males Bg and females Fg in 2007.

-

2

The central mortality rate m x,t g is calculated using a Lee-Carter model:

It is transformed into an annual mortality rate with the formula qg x,t =1-exp(m x,t g) In scenarios where mortality is reduced with a coefficient k, q x,t g is further multiplied by (1−k).

-

3

The population exposure and mortality for age x>0 in the following year is calculated using:

-

4

The number of fertile women is calculated using:

-

5

The number of live birth is calculated using:

-

6

The number of births (for x=0) in the following year is calculated using:

-

7

Migration is assumed to be +1 million; the adjustment for the population in cohorts is calculated using:

-

8

Return to step 1.

Legend

Rights and permissions

About this article

Cite this article

Zhavoronkov, A., Debonneuil, E., Mirza, N. et al. Evaluating the impact of recent advances in biomedical sciences and the possible mortality decreases on the future of health care and Social Security in the United States. Pensions Int J 17, 241–251 (2012). https://doi.org/10.1057/pm.2012.28

Received:

Revised:

Published:

Issue Date:

DOI: https://doi.org/10.1057/pm.2012.28